The 3-Pillar System in Switzerland

The Cornerstone of a Stable Pension System

The Swiss 3-pillar pension system is one of the best in the world. Through the interplay of state provision and private expenditure, a stable foundation can be built up over the long term, ensuring a high standard of living into old age. In this article, we explain exactly how the 3-pillar system works in Switzerland.

The 3 Pillars at a Glance

Each of the 3 pillars contributes its share to retirement planning. Here they are at a glance:

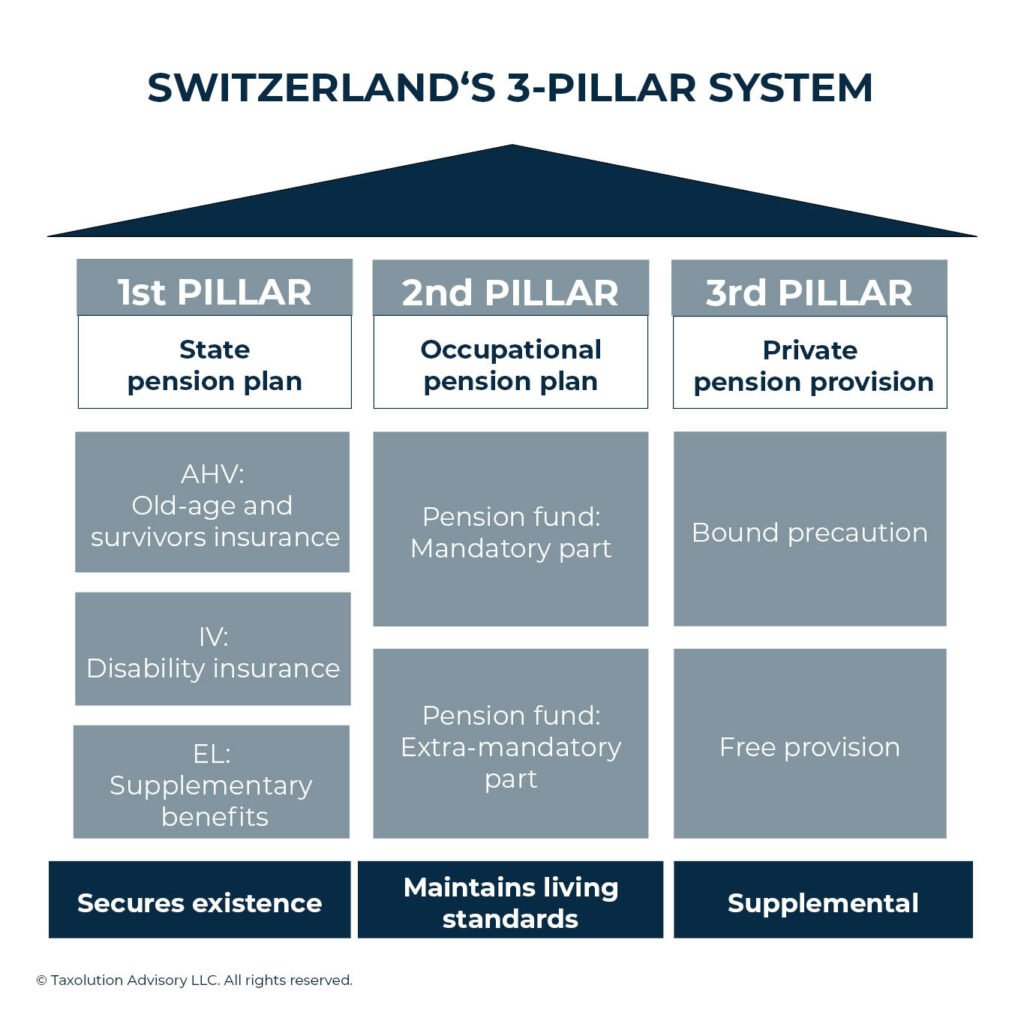

- State Pension Plan

The first pillar secures the existence. The pension scheme follows the principle of solidarity, in which both employed persons and their employers pay monthly contributions to finance today’s pensioners.

The main features of the 1st pillar are:

- compulsory for all who live or are employed in Switzerland

- financed by employees and employers

- Securing the minimum subsistence level

- Occupational Pension

The second pillar is the occupational pension, in which employees pay into a statutory pension fund and thus save up a credit balance over the course of their working life. This is paid out at the end of their working life.

The main features of the 2nd pillar are:

- mandatory for employees

- law requires certain minimum and maximum standards; employer have a wide scope of design to provide above-minimum benefits to its employees

- financed by employees and employers

- Ensures a standard of living above the subsistence level with pillar 1

- Private Pension Provision

The first and second pillars together should cover approximately 60% to 75% of the last gross salary. To close the remaining gap, private pension provision exists and gives employees the opportunity to provide for their old age on a voluntary basis.

The main features of the 3rd pillar are:

- voluntary supplementary provision

- financed by the employed person alone

- Together with pillars 1 and 2, ensures a continued high standard of living after employment

Pillar 1 in Detail: State Pension Plan

The first pillar in the Swiss pension system is made up of several small pillars, each of which covers a specific insurance:

- AHV: Old-Age and Survivors’ Insurance

The AHV has two goals:

- Securing basic material needs at the end of employment

- Securing basic material needs for surviving dependents (e.g. spouse or children) in the event of death

The AHV thus ensures that, after the end of the working life or in the event of the death of the employed person, sufficient financial means are available to secure the existence of the person concerned or their survivors.

The monthly contributions to the AHV are based on the income of the employed person and on the principle of solidarity: the full salary without any upper limit is subject to contribution whereas the benefits are limited between certain minimum and maximum standards.

- IV: Disability Insurance

The IV covers risks in the event of incapacity for work for health reasons. This means that if the employed person can no longer perform his or her usual work due to a permanent health condition or a health condition that has lasted for more than one year, the IV will provide financial benefits to mitigate the loss of earnings.

Affected persons have a duty to do everything possible to prevent disability, i.e. in consultation with doctors and other professionals, they must help to reintegrate them into the workplace – as far as their state of health allows.

- EL: Supplementary Benefits

All those whose AHV and IV benefits are not sufficient to cover the minimum costs of living are entitled to receive EL.

Rights and Obligations of the Person Entitled to Receive

Every employee resident in Switzerland contributes to the insurance in pillar 1. In the case of employment, the employee and employer share the contributions equally. Self-employed persons pay their contributions depending on their annual earned income. The obligation to contribute to AHV starts at the age of 17 and ends at the regular retirement age (for women at 64, for men at 65). Retirement age of women will be harmonized to age of 65 in the next few years. Temporary arrangements apply for certain age cohorts.

The amount of the AHV pension is based on the average income earned during the contribution years. The minimum amount in 2023 is CHF 1,225; the maximum amount is CHF 2,450.

Pillar 2 in Detail: Occupational Pension Plan

Employees automatically belong to a pension fund that the employer selects for them. In contrast to

the first pillar, where contributions are distributed to the beneficiaries on a pay-as-you-go basis, the

pension fund is based on the following principle: each person pays a contribution into the pension fund based on their salary, and in this way accumulates a credit balance over the course of their career.

Self-employed persons are not obliged to pay into the pension fund. However, they can do so on a voluntary basis.

The occupational pension plan consists of two parts:

- Mandatory Part

All employees are compulsorily insured from a minimum annual income of CHF 22,050 up to a maximum income of CHF 88,200.

The amounts paid in earn interest at a guaranteed minimum rate. - Extra-Mandatory Part

If the income is above the maximum amount, this is allocated to the extra-mandatory part, whereby these are voluntary benefits of the respective pension fund. The interest rate at which interest is paid on the credit balance can vary from pension fund to pension fund.

Before reaching retirement age, you can choose between a lump-sum withdrawal and/or a lifelong pension.

Contributions to pillar 2 are tax deductible and the funds accumulated are free of wealth taxation as long as the funds are not withdrawn. Credited returns or interests within the pillar 2 are not subject to income tax.

Pillar 3 in Detail: Private Pension Provision

Every employed person is free to make private provision in addition to the insurance in pillars 1 and 2.

The types of pension provision in Pillar 3 can be divided into two areas:

- Bound Precaution (referred as pillar 3a)

This means that early withdrawal of benefits is only possible under certain conditions. In return, however, the contributions paid in can be deducted from income tax (up to a maximum amount), which reduces the annual tax burden.

In addition, the capital saved hereunder is not subject to wealth tax, and withdrawals are taxed at a lower rate.

- Free Provision (referred as pillar 3b)

In contrast to restricted pension provision, unrestricted pension provision is not subject to any statutory regulations regarding the amount of payments and the timing of payouts. Depending on the insurance product selected, insured persons are merely bound by the terms of their contract with the insurer.

Do you have further questions about taxation or living in Switzerland? Contact us for a non-binding quote. We will get back to you promptly and discuss your individual situation.

Latest blog posts

Swiss Wealth Tax 2026: What Expats Need to Know

How much wealth tax will you pay in Switzerland? Compare 2026 cantonal rates with our interactive calculator, learn what’s taxable, and see how expats can reduce the bill.

Imputed Rental Value in Switzerland: What Property Owners Need to Know in 2026

In this article, we explain what the imputed rental value is, how it is calculated, and what all you need to take into account when declaring it in your tax return.

The 3-Pillar System in Switzerland in 2026: How Pillar 3a Works, What Changed, and How to Make the Most of It

A complete guide to Pillar 3a for expats and international professionals in Switzerland — contribution limits, tax savings, 3a bank vs securities, retroactive buy-ins, withdrawal tax by canton, and cross-border implications.