Principle of Family Taxation

In Switzerland, in addition to individual taxation for single taxpayers, there is also so-called family taxation. In this case, the income and assets of both spouses are added together and the tax rate for the entire family is then calculated from the total income and assets. This results in some special features, which we will discuss in more detail in this article. In addition, we will show you what options there are for saving taxes in family taxation.

Why Does Family Taxation Exist?

You may now ask yourself why there is family taxation at all. Doesn’t individual taxation suffice? Short answer: It does not necessarily.

If individual taxation were to apply to married couples, this would entail some problems that arise due to joint household management:

- It would be difficult to determine which income should be attributed to which of the two spouses. This would be even more difficult when allocating the assets.

- Through asset shifting and sham work, the couple could divide their assets and income between them in a way that reduces the tax burden for both of them.

For these reasons, joint assessment in the form of family taxation was introduced.

« Whereas previously both single persons filed a tax return separately and thus also paid tax on their income separately, from marriage on they file a joint tax return. The income and assets of both partners are added together and the tax rate is then determined. »

How Does Family Taxation Work?

Spouses or same-sex couples in a registered partnership are taxed jointly. The income and assets of both partners are added together and the tax rate is then determined.

The family taxation although is based on old social patterns, where single-earner households were much more common. One spouse earned all the income and the other partner was at home. This leads to overall more severe disadvantages for many couples, because the legal framework doesn’t fit our current structures anymore, where double-income households are rather the standard than the exception. But let’s dig deeper into the concept of family taxation itself:

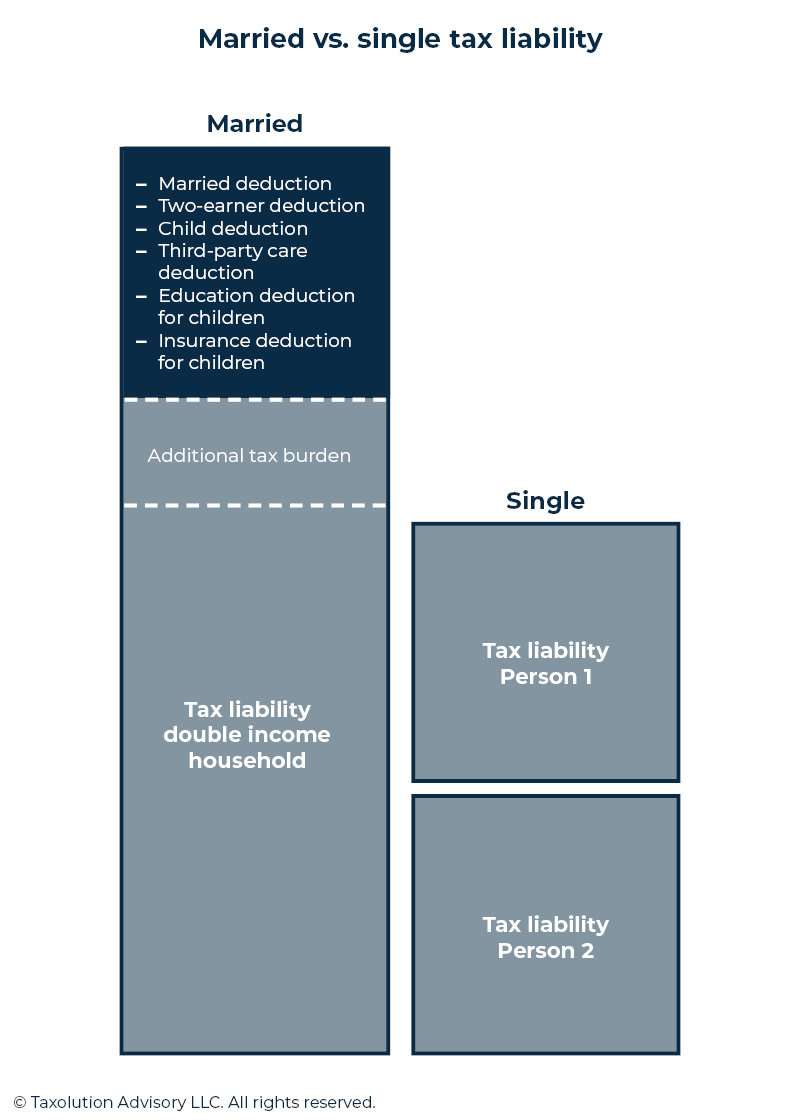

The disadvantage is that, due to the tax progression in Switzerland, the overall tax rate for spouses who earn roughly the same amount is higher than if they were to pay tax on their income and assets separately. This is why we also speak of a “marriage penalty” in Switzerland, find out more about it in this article.

The advantage of this is that any loss of income by one partner is offset against the income of the other partner, which then reduces the overall tax burden for both again. Furthermore, only one tax return has to be prepared.

Are Children Also Taxed?

The income of minor children is taxed separately from the parents’ income. The situation is different for any assets of the child: This is taxed together with the parents’ assets.

However, in many cantons there is a tax-free minimum for minors, which averages CHF 12,000.

Tax Breaks and Deductions for Married Couples

Many cantons offer married persons generous tax deductions to compensate for the disadvantages compared to individual taxation. The deductions are often even greater than those for single persons. Depending on the canton, the deductions are either fixed lump sums or amounts based on a percentage of the taxable income.

Married Deduction

This deduction is a lump sum (CHF 2,700, 2023) that can be deducted from the federal tax. In principle, all married persons may make use of it. In addition, there are various deductions that differ in type and amount depending on the canton.

Two-Earner Deduction

A married couple in which both partners have income may deduct half of the lower income from federal tax. There is an upper limit of CHF 13’600 and 8’300 (as of 2023). At cantonal level, there are sometimes very large differences in how much may be deducted from taxable income.

Child Deduction

The federal government and all cantons allow a tax deduction per child. The amount varies amongst the cantons.

In addition to the child deduction, in some cantons there is also the personal care deduction, which can be claimed if outside care is not possible or desired.

Third-Party Child Care Deduction

If childcare is used because the parents are employed or are unable to provide childcare for other reasons, the effective child care costs up to a maximum amount of CHF 25,000 (as of 2023) per child that has not yet reached the age of 14 may be deducted from the federal tax.

Education Deduction for Children and Young Adults

Both at the federal and cantonal level, families may make use of the education deduction. In some cantons, the deduction applies until the child reaches the age of 25 or 26. In other cantons, there is an income limit for the child’s income below which the education deduction may be claimed.

Insurance Deduction for Children

If one or both parents make alimony payments, one or both may still make use of the insurance deduction in addition to the child deduction. The deductible amount is CHF 700.

Parental Tax Rate

Single parents, widowers and separated or divorced persons who have custody of the children have tax relief in the form of the parental tax rate. Here, the rate for married persons is applied to the single person and a deduction of CHF 255 (as of 2023) per child is granted.

« Thus, the marriage does not have to be divorced yet for separate taxation to take place. It only has to be credibly proven to the authorities that one has separated. »

What Happens in Case of Separation or Divorce?

From the Date of Official Separation Individual Taxation

If a married couple separates, the partners are taxed separately as soon as the separation can be proven. In most cases, one of the two partners moves out and registers at the new place of residence. Separate taxation is then applied retroactively to January 1 for the current tax year.

Thus, the marriage does not have to be divorced yet for separate taxation to take place. It only has to be credibly proven to the authorities that one has separated.

Authorities recognize a marriage as separated if:

- at least one spouse lacks the will to continue the marriage

- the joint household no longer exists

- the means for housing and subsistence are provided by each of the spouses strictly individually and there is no longer any community spirit

Joint and Several Liability for Outstanding Taxes

Until the time of separate taxation, the two spouses are still considered jointly assessed. This means that the individual can still be prosecuted for the entire tax arrears.

Alimony

If there is an alimony obligation for one of the two former spouses after the separation or divorce, this must also be taken into account in the tax return of both persons:

- The debtor may deduct the alimony payments from his income

- The dependent must declare the alimony payments as income

What to Do if Not Everything Is Legally Settled Yet?

After separation or divorce, it can take several months to clarify all legal obligations between the two former partners.

Often it is then not possible to file a tax return because the former partners do not know who has to declare what on it.

Questions may arise such as:

- Who may claim which deductions for the children?

- Who is allowed to declare the parent rate?

In this case, ask the tax authority for an extension of the filing deadline. In some cases, you can also submit a provisional tax return, leaving open the items that have not yet been settled and submitting the issues in questions at a later date.

Do you have further questions about taxation in Switzerland? Contact us for a non-binding quote. We will get back to you promptly and discuss your individual situation.

Latest blog posts

Swiss Wealth Tax 2026: What Expats Need to Know

How much wealth tax will you pay in Switzerland? Compare 2026 cantonal rates with our interactive calculator, learn what’s taxable, and see how expats can reduce the bill.

Imputed Rental Value in Switzerland: What Property Owners Need to Know in 2026

In this article, we explain what the imputed rental value is, how it is calculated, and what all you need to take into account when declaring it in your tax return.

The 3-Pillar System in Switzerland in 2026: How Pillar 3a Works, What Changed, and How to Make the Most of It

A complete guide to Pillar 3a for expats and international professionals in Switzerland — contribution limits, tax savings, 3a bank vs securities, retroactive buy-ins, withdrawal tax by canton, and cross-border implications.