Marriage Penalty: What Impact Does Marriage Have on Taxation?

Update, February 2026: Switzerland votes on abolishing the marriage penalty through individual taxation on March 8, 2026. Read our full analysis with concrete CHF examples: Individual Taxation Referendum: What Expats Need to Know

In Switzerland, the marriage penalty refers to the potential tax disadvantages associated with entering into a marriage. In particular, high-earning married couples with two incomes are often worse off from a tax perspective than unmarried couples. In this article, we show you how the so-called marriage penalty comes about and present some calculation examples to illustrate the point. We will also show you what effects the marriage penalty has on the AHV pension and what tax benefits can be used so that the penalty is not quite so high.

Marriage Penalty in Switzerland

In the past, the taxation of married couples was less problematic than it is today. The reason for this was that there was a main earner (usually the husband) and a low earner, or a wife who took care of the children full time and did not work at all. Nowadays, however, it is the rule rather than the exception that both spouses work. Therefore, due to joint taxation in a marriage, this sometimes leads to disadvantages, especially if both partners earn very well and approximately the same amount.

«In the case of married couples, a joint assessment is prepared. This means that the incomes of both spouses are added together and then a single tax rate is determined, at which the total income must be taxed.»

Progressive Taxation in Marriage Is an Obstacle

The reason for the marriage penalty is progressive taxation in Switzerland: the higher the income, the higher the tax rate applied to it. If a couple is unmarried, both partners are assessed individually. This means that each partner files his or her own tax return and a tax rate is determined according to his or her income at which income and assets must be taxed.

In the case of married couples, a joint assessment is prepared. This means that the incomes of both spouses are added together and then a single tax rate is determined, at which the total income must be taxed. And this is where things can get problematic: If both spouses earn approximately the same amount, the joint assessment results in a higher tax rate than if both partners were assessed separately.

If there is only one main earner in the marriage, the problem does not exist, which is why this taxation model was not considered unfair in the past, since married couples were not in a worse position for tax purposes than unmarried couples. For high-income dual earners, on the other hand, this is now referred to as a marriage penalty, because the disadvantages can be severe.

Disadvantages for AHV Pensions

Not only in taxation, but also in AHV pension disadvantages arise for pensioner couples. They receive only 150% of the maximum pension. If they were not married, each of the partners would receive 100% of the maximum pension, so that the joint household would have 200% of pension money at its disposal.

Although married couples have to pay less into the AHV, this results in disadvantages later on when drawing the pension, if both partners have always paid in the maximum rate. This makes pensioner couples even consider getting divorced and continuing to live together in concubinage so that they can get more from their pension.

The Additional Tax Burden on Two-Earner Married Couples: Some Examples

Using several examples, we want to show you how the taxation of married and unmarried couples differs in some cantons.

Therefore, We Have Considered the Following Cases:

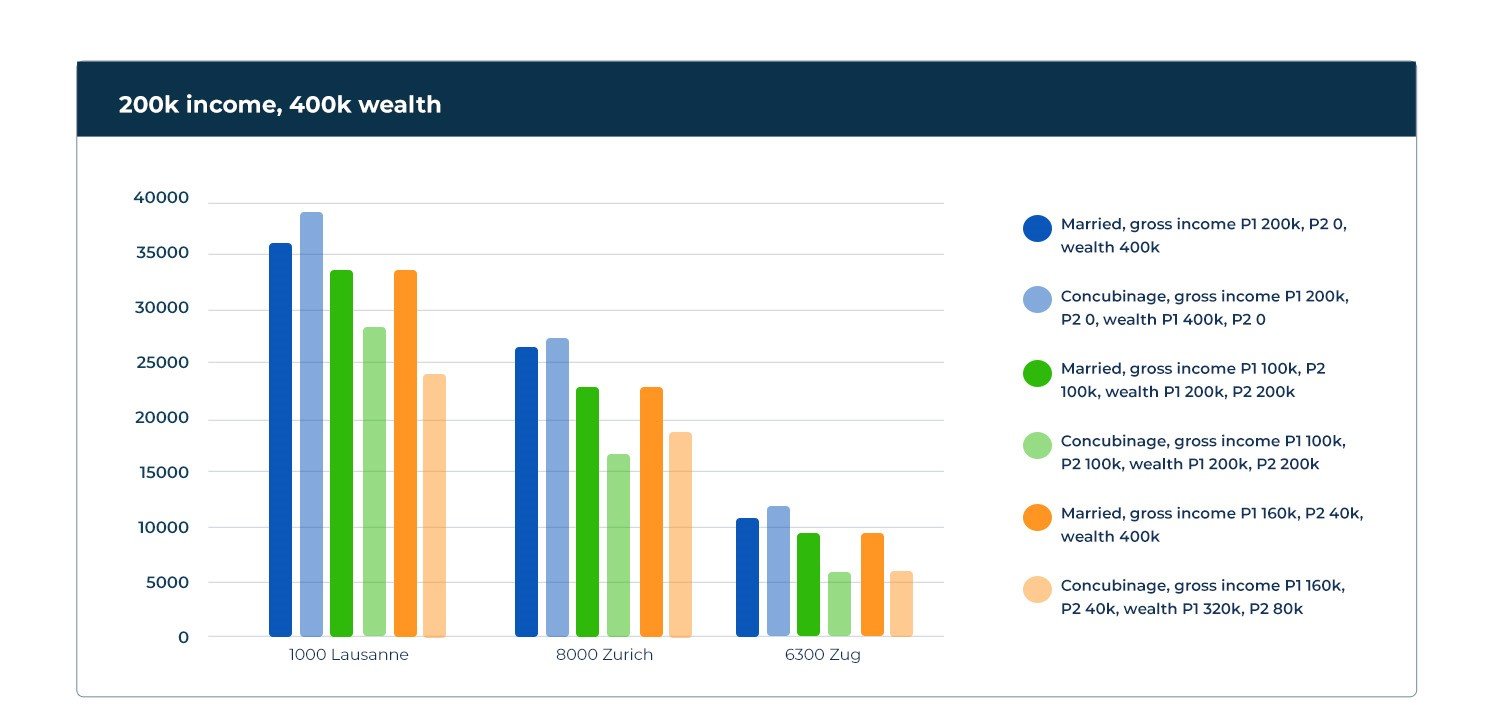

- Total income in the household: CHF 200,000 and assets of CHF 400,000.

- Total household income: CHF 500,000 and assets of CHF 1 million

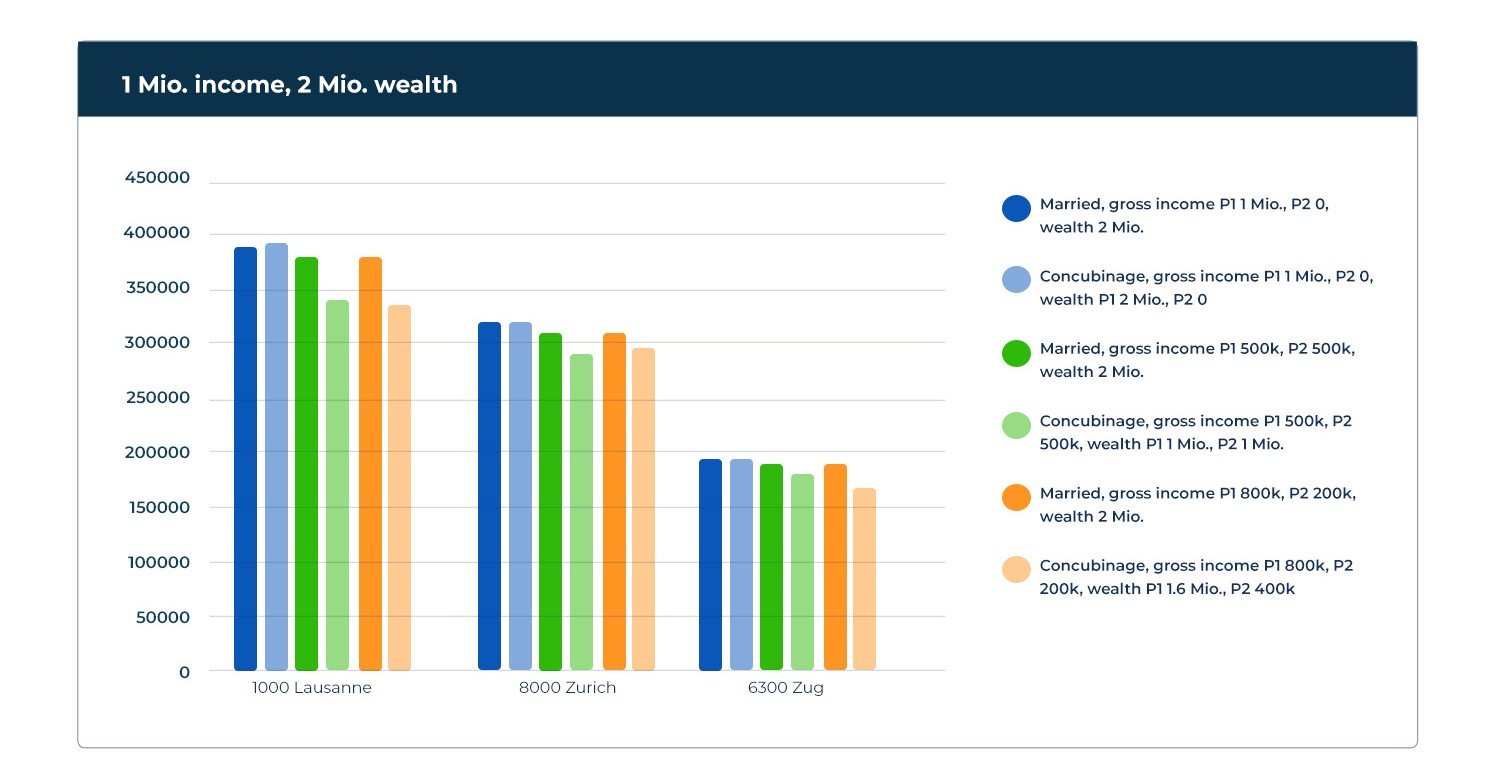

- Total household income: CHF 1 million and assets of CHF 2 million

We Performed the Calculation for the Following Cities:

- Lausanne

- Zurich

- Zug

We have created different scenarios regarding marital partnership or concubinage with different income and asset compositions, each calculated using the example of 2 children:

- Married, one partner earns all income

- Concubinage, one partner earns all income

- Married, both partners with equal income and assets

- Concubinage, both partners with equal income and assets

- Married, one partner as main earner, the other as low earner

- Concubinage, one partner as main earner, the other as low earner

Interpretation of the Results

Within the different income scenarios, the first thing to note is that the tax burden differs significantly between cities. In Lausanne, the tax burden is higher than in Zug in all scenarios.

Progressive Taxation as the Biggest Disadvantage in the Case of Marriage

If we look at the income scenario with a total income of CHF 200,000, it is noticeable that in all cantons the tax burden is highest for the case of a couple in concubinage where only one of the partners has an income. In all income classes, this is the only case where married couples have an advantage. This is due to higher social deductions for married tax subjects, which was intended to relieve single-earner households, as they used to be common.

In comparison, there is an advantage for married couples where one of the partners is a low earner: despite the same total household income, the tax burden is lower, as there are tax deductions intended to reduce the impact of the marriage penalty. This effect is observed in all locations.

Concubinage vs. Married Couple

In the case of cohabiting couples, both partners are assessed individually. Thus, the total tax burden in the household is made up of the two individual tax burdens, which in turn depend on the level of income and assets.

It can be seen in all double-income examples that the tax burden for a cohabiting couple is always lower than for a married couple, regardless of whether both earn the same amount or only one of the two is the main earner.

Depending on the canton in which the two cohabiting partners are taxed, there may also be differences in exactly how the two individual incomes are taxed.

Let’s take a look at the CHF 200,000 scenario: In Lausanne, the total tax burden for the household is higher if both partners earn the same amount than if only one is the main earner. However, if these two partners lived in Zurich, the tax burden would be higher for the couple with the main and low earner.

Result: Tax Disadvantaged by Marriage Penalty

Based on the above examples, it is clear that progressive taxation is a disadvantage for high-earning married couples with double incomes, as the tax rate for the joint income is higher than for the two individual incomes. Partners who are not married have a distinct advantage here.

Single-Earner Households

Married couples with a sole earner without children have an advantage over childless couples with a sole earner living in concubinage, as they benefit from the married tax rate, which is advantageous compared to the single rate that applies to both unmarried partners. This effect vanishes again for single-earner households with children, since having children grants the main earner the married tax rate regardless of marital status.

Is It Possible to Avoid the Marriage Penalty?

High-earning couples who are not married can consider whether or not they want to marry. There can be considerable differences depending on the canton. If you are married, or if you absolutely want to get married, you can also take advantage of tax benefits that only apply to married couples and are intended to mitigate the marriage penalty somewhat:

- Second-earner deduction: half of the lower income may be deducted from the federal tax (maximum CHF 13,400, minimum CHF 8,100). Depending on the canton, other deductions apply.

- Married couple deduction: A lump sum of CHF 2,600 may be deducted from the federal tax. There are other deductions at the cantonal level, but these minimize the marriage penalty only marginally.

Conclusion: Marriage Penalty as a Disadvantage for High-Earning Couples

As we have now seen, the tax burden is higher for high-earning married couples with double income than for unmarried partners with the same income. This presents couples with the question of whether to marry at all, and if so, by how much the tax burden will increase.

Since taxation varies greatly from canton to canton and there are many factors that all affect taxation, depending on the income and asset constellation, it is not possible to make a blanket statement. Of course, many other factors also play a role. Depending on the situation, marriage can be quite a sensible overall package; the marriage penalty is only one specific tax disadvantage in the grand scheme of things.

Therefore, from a tax perspective, couples should carefully calculate how marriage will affect their future tax situation. Depending on how high the marriage penalty turns out to be, it can be decided whether this factor is relevant for the decision or not.

Tax Return Cost Calculator

Do you seek a quick idea of the cost of our tax return service? If we have sparked your interest, you can send it to us without reservations, as it is a non-binding request. We will contact you promptly to discuss your situation with you.

Latest blog posts

Swiss Expat Tax Benefits 2026: Special Tax Deductions for Posted Employees

In this article, we explain what the special “expat” status is all about, how an expat differs from other employees in Switzerland, and what benefits you can derive from it if you also belong to this group.

Is Switzerland Still a Tax Haven in 2026? How Much You Actually Pay vs the EU, UK, UAE & Monaco

Switzerland isn’t classically a tax haven, but for high earners the structural mix beats every EU comparator. Take-home and wealth tax compared to UAE, Monaco, UK, Germany, Italy, more.

Swiss Pillar 2 Buy-In 2026: Tax Savings, the 3-Year Withdrawal Block, and When It’s Worth It

Many pension funds advertise voluntary purchases and present attractive calculation models to interested parties. What is often not mentioned is that the voluntary purchase into the pension fund is not worthwhile for everyone and does not always help with tax savings.