Tax Consequences of Divorce or Separation

A divorce or separation is not an easy undertaking for all parties involved, as it represents a serious break in the lives of both partners (and possibly their children). Many things have to be (re)organized, there are administrative procedures to be dealt with, as well as the move of one of the spouses to another apartment.

Sooner or later, the question inevitably arises as to what effects the divorce will have on the taxes to be paid. There is always a lot of uncertainty here, because there are many things to consider when you leave the joint assessment and are henceforth subject to the single assessment again. Here we clarify the most important questions that you will have to deal with from a tax law perspective if you want to get divorced or have already done so.

« The timing of the separation can therefore have significant consequences for the tax burden of the individual.»

From When Does the Separate Assessment Apply?

If you are separated at the end of the tax period of the respective year (December 31), the separate assessment applies retroactively for the complete tax year. This means that the now separated former spouses each file their own tax return, and no longer a joint one as before.

The timing of the separation can therefore have significant consequences for the tax burden of the individual. So if things are separating “on good terms”, it is advisable to time the separation in such a way that the tax consequences are compatible for both partners.

When Is One Considered Separated?

Time and again, ambiguities arise as to the point at which one is actually considered separated. Because even before the formal divorce, the partners can be considered separated if the following criteria are met:

- At least one of the partners lacks the will to continue the marriage or partnership

- The common household is canceled

- There is no longer any community for housing and living expenses

Thus, anyone who has not yet received a formal divorce decree, but who meets the above criteria, is nevertheless already considered separated.

Written proof of separation or a legal ruling is not necessary if it can be credibly conveyed to the tax authority that one has separated. It is usual to present a tenancy agreement or registration certificate from the new residence authority showing that one of the partners no longer lives in the previous joint household.

All these regulations apply to both married couples and registered partners.

What Happens to the Taxes Already Paid or Owed in the Separation Year?

Until the time of separate taxation, joint and several liability for taxes applies to the former spouses. This means that if there is a repayment of overpaid taxes, most cantons will refund half of the amounts (or pro rata in relation to the total tax) to each person. Federal tax, on the other hand, is usually refunded to the person who paid it. It is important to note that there is no longer a joint account at the tax office here, but each individual has a separate account.

The same also applies to taxes still owed: Here, the former spouses are made liable to pay according to their share of the total tax.

How to Fill in the First Tax Return After Separation?

When everyone has to fill out a separate tax return again, there are often further ambiguities, since divorce proceedings are often still ongoing, or legal matters need to be clarified. For example, there are questions about custody of the children, alimony payments, or the division of previously joint property (such as residential property).

All these things also have an impact on the tax return (and the taxes to be paid). Both spouses must therefore make sure that the tax returns do not contradict each other.

If at the time of the due date for the tax return not everything has been clarified so that the two individual tax returns can be completed without gaps, it is advisable to ask the tax authority for a postponement of the submission deadline. It is also possible to file a provisional tax return and leave the items that still need to be clarified open, and then submit them later.

Which Tax Rate Applies After the Divorce?

For childless persons, the tariff for single persons applies after the divorce.

If the couple has dependent children, or lived with a person in need of support in the household, the situation becomes somewhat more complicated. Depending on with whom the child or the person in need of support will live, the partner may tick the more favorable family tariff. The other partner then ticks the tariff for single persons. In addition, it must be clarified who may indicate child or caregiver deductions in their tax return.

Maintenance Payments in the Tax Return

If alimony is paid, the person who pays it may deduct it from his or her income. The person who receives the alimony, on the other hand, must add it to his income.

Not only monetary payments can be understood as maintenance, but also payments of a material nature, e.g. if one of the partners leaves the apartment to the other and the child.

Such benefits must be clarified with the canton of residence as soon as possible so that these circumstances are known to the authorities and there are no inconsistencies in the tax returns.

Does Withholding Tax Have to Be Paid Again?

If one is married to a Swiss citizen or a person with a permanent residence permit (Permit C), any withholding tax for the other person does not apply.

However, in case of separation, this person will be taxed at source again, starting from the month after the separation. Withholding taxation is waived again only if the person liable to withholding tax receives alimony payments.

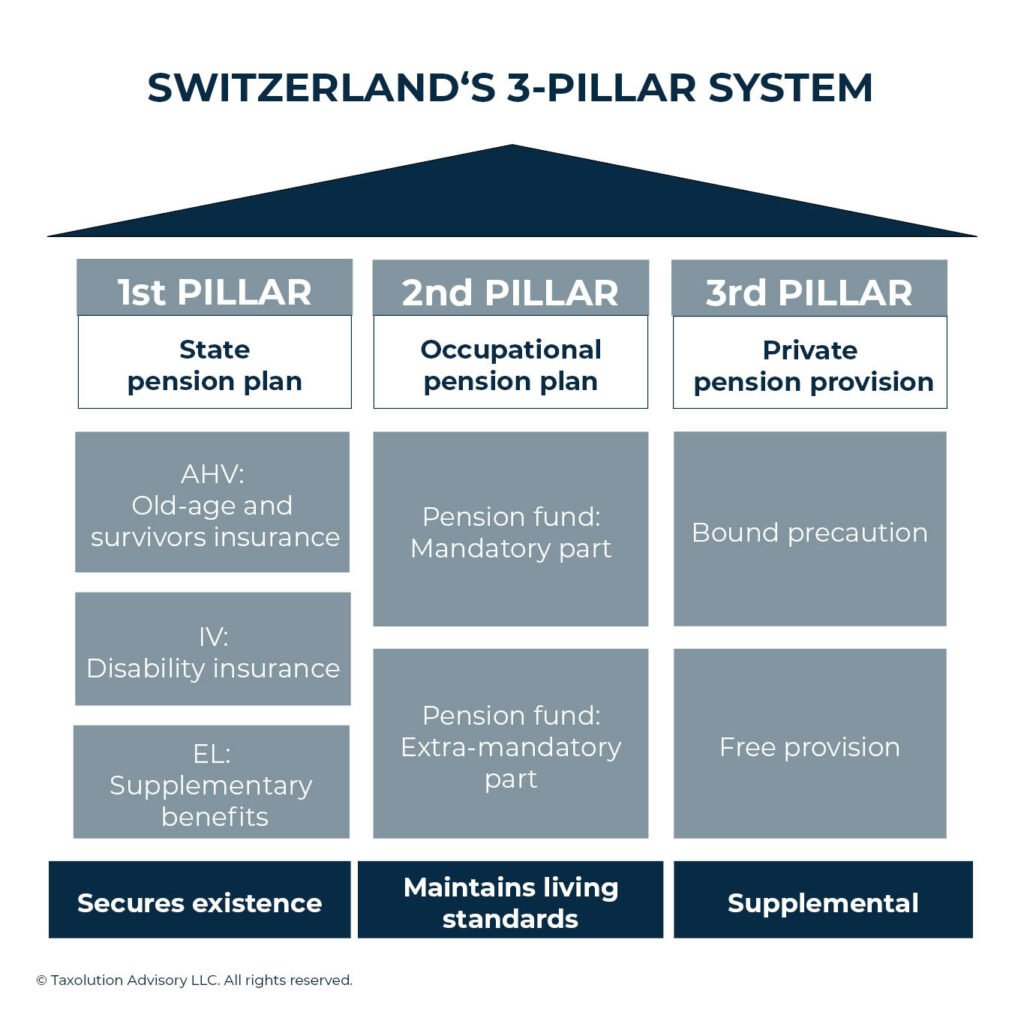

What Happens to the Joint Social Security and Pension Holdings?

Pillar 1

The OASI (old-age and survivors’ insurance) assets accumulated during the marriage are divided equally between the OASI accounts of the two former partners. In order for splitting to take place, a corresponding application must be submitted to the compensation office.

Pillar 2

Pension fund assets are also divided equally between the divorced persons. The total credit balance is the amount saved from the date of marriage to the date of separation. Interest is also taken into account.

A possibly agreed separation of property before the marriage has no effect on the splitting of the credit balance from the pension fund, but only applies to credit balances paid in before the marriage.

As a rule, the division results in pension gaps for both spouses. These can be closed by a tax-privileged purchase.

Pillar 3

In the case of private pension provision, the agreements regarding the separation of property in the marriage contract are decisive. If no prenuptial agreement has been concluded, the accumulated assets are divided equally. Other division ratios are also possible or the waiver of division if the separated persons agree to this. If the division is waived, it should be noted that capital tax is due when the Pillar 3a assets are paid out.

Do you have further questions about taxation in Switzerland? Contact us for a non-binding quote. We will contact you promptly and discuss your individual situation.

Latest blog posts

Swiss Expat Tax Benefits 2026: Special Tax Deductions for Posted Employees

In this article, we explain what the special “expat” status is all about, how an expat differs from other employees in Switzerland, and what benefits you can derive from it if you also belong to this group.

Is Switzerland Still a Tax Haven in 2026? How Much You Actually Pay vs the EU, UK, UAE & Monaco

Switzerland isn’t classically a tax haven, but for high earners the structural mix beats every EU comparator. Take-home and wealth tax compared to UAE, Monaco, UK, Germany, Italy, more.

Swiss Pillar 2 Buy-In 2026: Tax Savings, the 3-Year Withdrawal Block, and When It’s Worth It

Many pension funds advertise voluntary purchases and present attractive calculation models to interested parties. What is often not mentioned is that the voluntary purchase into the pension fund is not worthwhile for everyone and does not always help with tax savings.