Income and wealth taxation

04

Income and

wealth taxation

Income tax

Swiss income tax is levied on the individuals worldwide income such as (self-) employment, pension and retirement income, immovable as well as movable assets, lottery winnings.

Requirements for tax residence in Switzerland

In the civil law sense, domicile represents the place where a person has his permanent residence with the intention to remain there. This residence therefore represents the center of the person’s life.

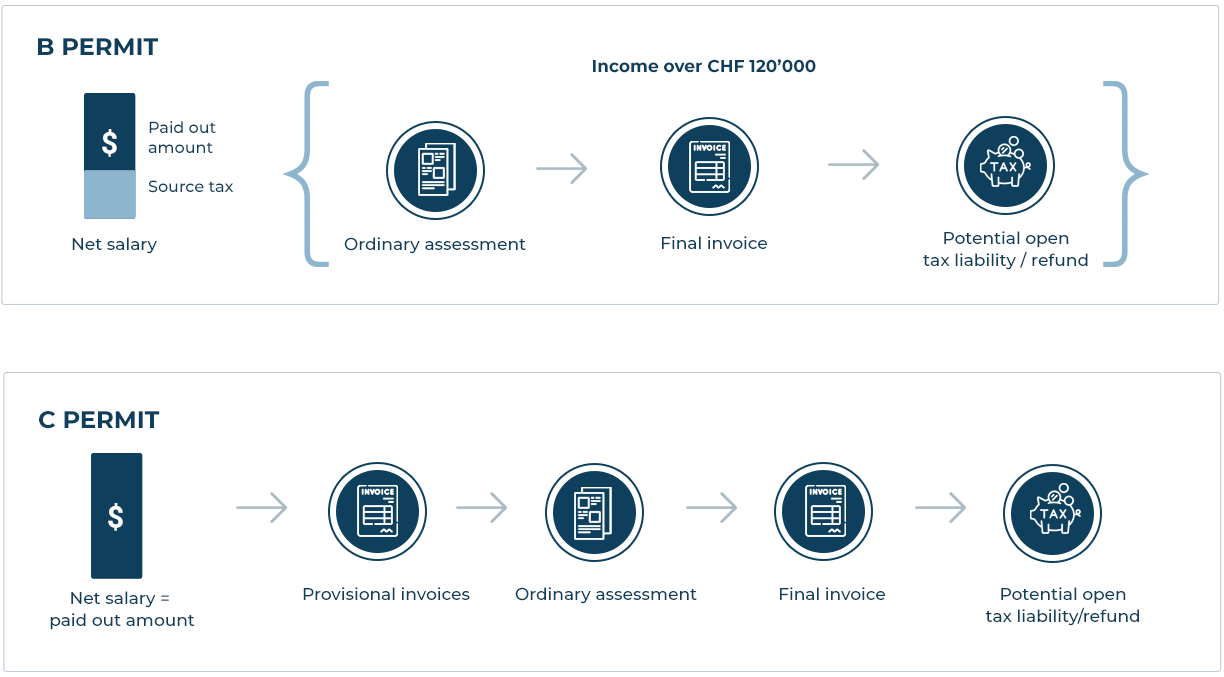

B and C cards decide how to pay the tax

If you want to work in Switzerland as a foreigner, you need either a residence permit (B permit) or a settlement permit (C permit). Depending on which of the two one receives, this has an impact on the way taxes are paid.

Residence permit (B permit)

- Employment relationship: There is an employment contract that is limited or unlimited to at least one year.

- Self-employed persons: proof of effective self-employment

Settlement permit (C permit)

- The employed person has lived in Switzerland for more than five years (without interruptions).

Paying taxes as a B permit holder

Anyone who holds a B permit and is gainfully employed pays withholding tax in Switzerland. This means that the employer deducts the monthly tax contributions to be paid from the salary and passes them on directly to the tax authorities. Thus, the principle of withholding taxation differs from “ordinary” taxation in Switzerland, where taxpayers receive their gross salary and are required to submit a tax return once a year and then pay the taxes to the tax authorities themselves. Exception: Anyone with an annual salary of more than CHF 120,000 does not only pay withholding tax, but submits a tax return with the tax authorities in retrospect according to the “ordinary” system. The withholding tax payments will only function as prepayments in these cases.

Paying taxes as a C permit holder

If the employed person has a C permit, they pay taxes in the same way as a Swiss citizen: per monthly or quarterly advance tax payments (regulated differently depending on the canton) through provisional tax invoices. The tax rates vary greatly from canton to canton.

At the end of the year, it is obligatory to file a tax return, which then determines exactly how much tax the employed person actually has to pay. This can result in a plus or a deficit, so that either the overpaid taxes are refunded by the tax authorities, or the taxpayer has to pay additional taxes.

Taxable income

- Employment income

- Rental income

- Pensions

- Alimony/child support received payments

- Investment income

- Self-employment profits

- Family allowances

- Unemployment & other insurance benefits

Social security on income tax

Since security contributions are usually paid in the country where the work is performed, foreigners working in Switzerland are obliged to contribute to the social security system (AHV/IV/EO, BVG, UVG) which builds the first out of the three pillars in the Swiss social security system. It includes age, accident, survivor as well as invalidity pensions. The contributions for the first pillar of total 10.25 % is covered half be the employer and half by the employee.

Wealth tax

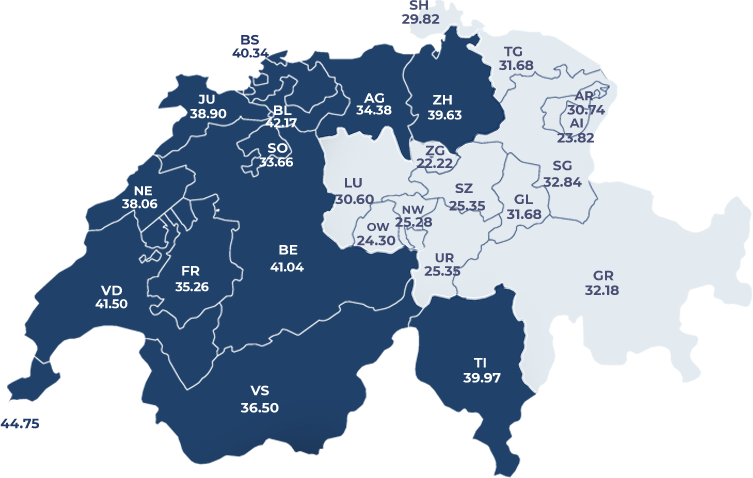

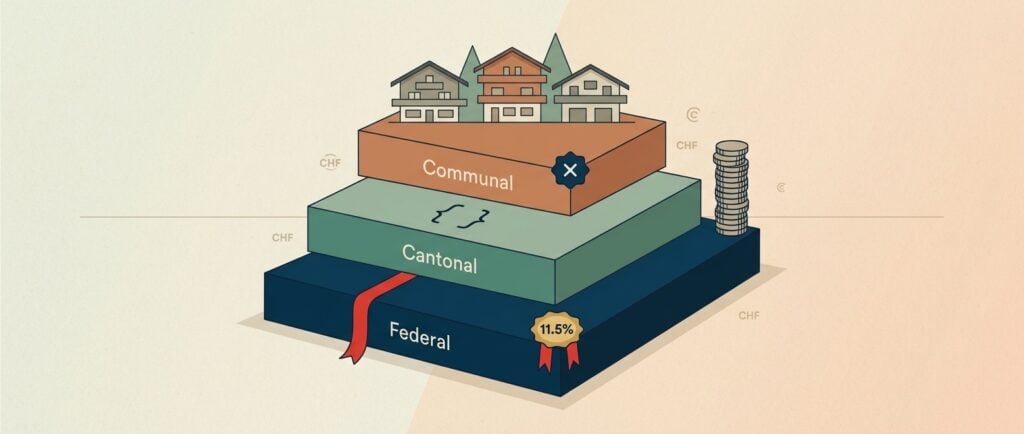

Wealth tax is independent of income, and thus not linked to income tax. It therefore only assesses the taxpayer’s assets. The 26 cantons and the municipalities each have their own tax rate for wealth tax. So, depending on where you reside, the tax rate can vary, and ranges from 0.13% to 1.1%. The taxation is progressive, i.e. as the wealth increases, so does the tax rate.

What all falls under the taxable assets?

All assets of the taxpayer – both domestic and foreign assets – are subject to wealth tax.

- Cash (if this exceeds the normal household cash holdings)

- Shares and fund units (domestic and foreign)

- Precious metals: gold, silver, platinum

- Bank account balances

- Private equity like GmbH/AG shares

- Granted loans (lender declares it as an asset, borrower as a debt)

- Life insurances (if surrenderable and not in tax pillar 2 or 3a)

- Usufructuary rights (e.g. lifelong right of residence)

- Domestic real estate and land

- Land and water vehicles of all types (except leased vehicles)

- Valuable collections and objects (art pieces, stamps, coins, wine and spirits, jewelry, valuable musical instruments)

- Farm animals and horses

If you have further questions about taxation in Switzerland, feel free to contact us for a non-binding quote, as this is our core competence. We will contact you promptly and discuss your individual situation.

Latest blog posts

Swiss Pillar 2 Buy-In 2026: Tax Savings, the 3-Year Withdrawal Block, and When It’s Worth It

Many pension funds advertise voluntary purchases and present attractive calculation models to interested parties. What is often not mentioned is that the voluntary purchase into the pension fund is not worthwhile for everyone and does not always help with tax savings.

Swiss Income Tax Rates 2026: Federal, Cantonal & Communal Stack Explained

Swiss income tax in 2026: federal brackets, the 26-canton effective-rate table at CHF 250k single and CHF 350k married, and the canton-choice CHF lever.

Swiss Property Maintenance Tax Deductions 2026: Last Window Before the 2029 Eigenmietwert Switch

Flat-rate vs actual costs, the 26-canton matrix, and the 2026-2028 last window before the Eigenmietwert switch ends federal maintenance deductions in 2029.