Managing Healthcare Costs & Autism in Switzerland: A Tax Perspective

Navigating healthcare expenses in Switzerland can be complex due to mandatory health insurance and multifaceted tax regulations. However, if you know how to structure and claim these costs, you can significantly lower your financial burden—whether it’s for routine medical needs or specialized autism-related therapies, devices, and support services. Because federal and cantonal rules vary widely, staying informed is essential to make the most of your available deductions.

This guide provides a structured overview of tax deductions for healthcare expenses in Switzerland. It starts with the foundational rules on mandatory health insurance premiums, clarifies which out-of-pocket costs are eligible, and explains key cantonal differences. It then looks at autism-specific tax considerations, including how disability status may affect potential benefits. Throughout, the aim is to offer a realistic snapshot rather than definitive statements, since both federal and cantonal rules can change and may require additional documentation. If your case is complex or falls into a gray area, it’s worth examining the relevant regulations in detail to ensure accuracy.

How to Deduct Health Expenses from Taxes

When navigating healthcare-related tax deductions in Switzerland, start by familiarizing yourself with two main categories:

- Insurance premiums

- Actual medical expenses

Although federal and cantonal laws provide avenues to claim these costs, the specific rules can be intricate. Be mindful of percentage-based thresholds (such as the common 5% of net income requirement for self-paid medical costs in many cantons), maximum deductible amounts, and any required documentation. Before you file, it’s crucial to gather all relevant paperwork—particularly your annual tax statement from your insurer and any itemized invoices or receipts.

Tax Statement

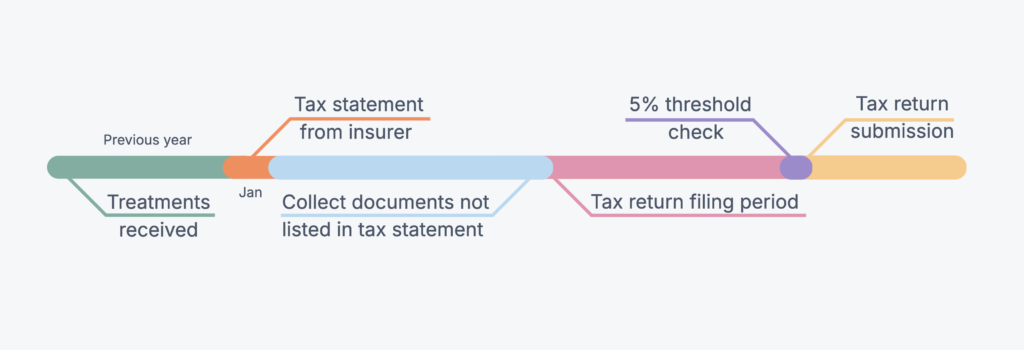

Toward the end of January, Swiss health insurers issue a tax statement summarizing your payments for the previous year. This statement includes all the premiums you’ve paid (basic and supplementary), any premium reductions you’ve received, and a record of out-of-pocket expenses that were partially or fully covered by insurance. Keep this document readily available—it is your primary reference when completing the healthcare-related sections of your tax return. Ensure the data is accurate and cross-check it with your own receipts to confirm you’re claiming the correct amounts.

Health Insurance Premiums

Health insurance premiums are often one of the largest recurring expenses in Swiss households. While you can usually claim them as deductions, the extent of these deductions varies at both federal and cantonal levels.

Federal Regulations

At the federal level, you can deduct a set amount for health and accident insurance premiums. Previously, unmarried taxpayers could deduct a minimum of CHF 1.700, while married couples filing jointly could deduct CHF 3.500, though these amounts are subject to change. For example, as of 2025, the limits will increase to CHF 1.800 for unmarried taxpayers and CHF 3.600 for married couples. Additionally, if you’ve made no contributions to pillar 3a or your pension fund, you can deduct CHF 2.700 (singles) or CHF 5.400 (married). For further details, visit the Swiss Federal Tax Administration.

Cantonal Variations

Each canton sets its own deductible limits for health insurance premiums. For example, the canton of Vaud currently allows single taxpayers to deduct up to CHF 4.900 and married couples up to CHF 9.800 for the 2024 tax year. Zurich, by contrast, imposes lower limits.

| Canton | Single Taxpayer | Married Couple (joint) |

| Vaud | CHF 4.900 | CHF 9.800 |

| Zurich | ~ 2.600-3.000 | ~ 5.200-6.000 |

| Bern | ~ 3.000-3.500 | ~ 6.000-7.000 |

| Geneva | ~ 3.000-3.500 | ~ 6.000-7.000 |

Out-of-Pocket Medical Costs and the 5% Threshold

Separate rules apply to out-of-pocket medical expenses, which you can typically deduct only if they exceed a certain percentage of your net income—often 5%—with any amounts above that threshold qualifying for a deduction.

Example: A High-Income Household

Consider a household with a net income of CHF 250.000. Under a 5% threshold for out-of-pocket medical expenses, they must exceed CHF 12.500 (5% of 250k) before any costs become deductible. If they spend CHF 14.000 on eligible medical bills, they can claim CHF 1.500 (the amount above CHF 12.500). It is important to note that this threshold applies strictly to self-paid healthcare costs rather than to health insurance premiums—covering, for instance, dental treatments, procedures abroad not covered by Swiss insurance, and fees for retirement or nursing homes. Although the family in this example exceeds the threshold, their tax deduction remains relatively modest, underscoring how even substantial healthcare bills can lead to only limited tax savings at higher income levels.

Because many households never exceed these thresholds—especially at higher income levels—they receive no tax benefit for out-of-pocket costs. The exact rate also varies by canton; while a 5% rate is common, Geneva uses 0,5%, and Valais (VS), St. Gallen (SG), Glarus (GL) use 2%, making it easier to claim at least some deduction on moderate medical expenses in those regions.

Who Can You Deduct Premiums for?

Health insurance premiums for yourself, your spouse, and any dependent children typically qualify for deductions up to prescribed limits. At the federal level, you can often claim an additional allowance per child (e.g., CHF 700), but this figure may be higher or lower depending on your canton. For example, Zurich imposes a maximum of CHF 1.300 in additional deductions.

Other Deductible Healthcare Costs

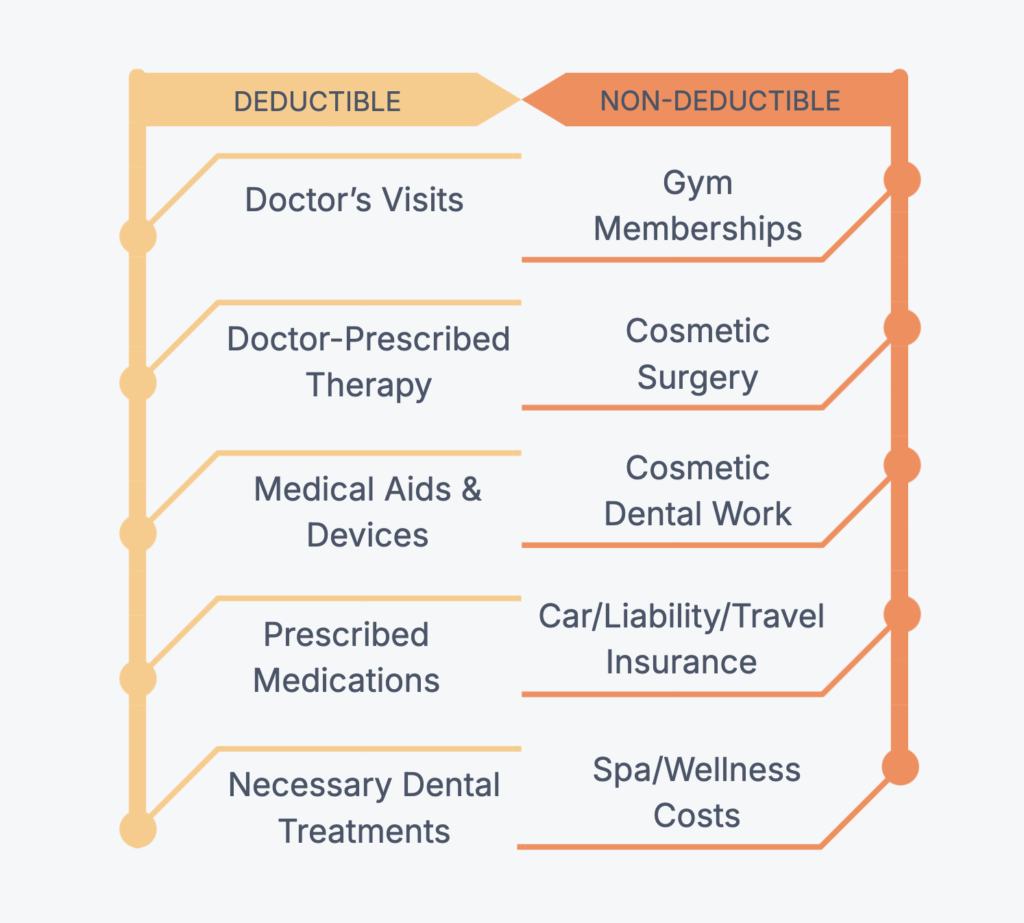

Beyond insurance premiums, Swiss tax laws may allow you to deduct a variety of healthcare expenditures—provided they are deemed medically necessary and meet threshold requirements:

General Medical Treatments

Costs for services rendered by recognized medical professionals (e.g., doctors, official naturopaths) can be deducted.

Medications and Vaccinations

- Prescribed Medication

To qualify for deductions, medications must be prescribed by a doctor.

- Vaccinations

Preventive care like vaccinations is also included in deductible expenses.

- Medical Aids and Devices

Covers the cost of aids that enhance quality of life or restore functionality, such as glasses, contact lenses, hearing aids, and prostheses.

Long-Term and Elderly Care

Deductible costs include ongoing care services such as Spitex (home care), as well as fees for old people’s homes or nursing homes.

Doctor-Prescribed Diets

If a specific diet is prescribed by a doctor to manage a medical condition, these costs are also eligible for deduction.

Specialized Medical Procedures

- Breast Reduction

Eligible when medically necessary due to health impairments like chronic back pain.

- Hormone Treatments and Fertility Services

Includes hormone therapy, artificial insemination, and in vitro fertilization, provided these treatments are prescribed by a healthcare professional.

Non-Tax-deductible Healthcare Costs

Despite the broad range of deductible healthcare costs, Swiss tax authorities draw a clear line around certain categories. If you’re unsure whether a specific procedure is purely aesthetic or genuinely medically necessary, start by discussing its necessity with your healthcare provider and collecting relevant documentation. You can then include the expense in your tax return, accompanied by a clear justification. Keep in mind that tax offices may request additional evidence or details before deciding whether to accept the claim.

- Cosmetic Surgery

Procedures performed solely for aesthetic purposes, such as facelifts, liposuction, or other beauty-enhancing surgeries, are not tax-deductible. These are classified as elective treatments and do not meet the criteria for medical necessity.

- Wellness and Fitness

Expenses for gym memberships, yoga classes, spa treatments, or other wellness activities aimed at general health or relaxation are not deductible. While beneficial for well-being, they don’t qualify as medical care under tax regulations.

- Non-Healthcare Insurance

Premiums for car insurance, liability insurance, household contents insurance, travel insurance, and property insurance are not eligible for tax deductions. These types of insurance protect personal assets rather than health and are therefore excluded.

What about Dental Costs?

Dental work in Switzerland can be expensive, but certain treatments may qualify for deductions if they serve a medical (as opposed to purely cosmetic) purpose. For example:

- Essential Dental Treatments

Fillings, root canals, and extractions typically meet the medical necessity threshold.

- Orthodontic Treatment

Braces or aligners can be claimed when prescribed for functional or structural issues.

- Dental Hygiene

Routine cleaning or scaling may be deductible if recommended by a dentist and not merely elective.

- Dental Appliances

Dentures, crowns, and implants are often considered medical necessities.

- Non-Deductible Cosmetic Treatments

Cosmetic procedures like teeth whitening or bleaching are not deductible. These treatments are classified as aesthetic enhancements, which fall outside the scope of medical necessity.

Navigating Taxes for Individuals with Autism in Switzerland

Autism spectrum disorders can qualify for certain disability-related tax relief measures in Switzerland, but the specific benefits and recognition procedures vary by canton. Broadly, if the condition is recognized as a disability, costs for therapies, educational programs, or specialized tools may be partially or fully deductible. However, families should be prepared for possible documentation requirements—such as official medical evaluations or disability insurance (IV/AI) rulings—to substantiate the claim. Moreover, not all autism-related expenses automatically qualify; you may have to prove that the costs go beyond standard educational or medical needs and address recognized therapeutic objectives.

Autism and Disability Status

Autism is widely acknowledged as a developmental condition, often included under disability legislation in multiple countries. In Switzerland, the recognition of autism for tax purposes typically hinges on fulfilling criteria set by the disability insurance (IV/AI) or local medical boards. While international frameworks like ICD-10 (soon to be replaced by ICD-11) influence how autism is classified, Swiss tax authorities focus on local legal definitions. Depending on the severity of the condition and official disability recognition, the individual or family may be eligible for additional deductions, provided they can supply consistent evidence of medical need and documented expenses.

Swiss Legal Framework for Autism

In Switzerland, autism-related expenses are often classified under disability-related costs for tax purposes. For example, in the canton of Zurich, the Zürcher Steuerbuch (ZStB) 32.1 outlines that these costs are deductible without a self-retention threshold, unlike general medical expenses, which must exceed 5% of net income to qualify for deductions. This classification allows expenses such as specialized therapies, educational support, and assistive devices to be partially or fully deducted, offering significant tax relief.

Tax Savings Opportunities for Autism-Related Expenses

While certain autism-related expenditures (e.g., specialized therapies, educational support, and assistive communication devices) may be deductible, the rules are not uniform across Switzerland. Typically, costs linked explicitly to medically certified treatments or structured educational programs stand the best chance of qualifying.

- Special Education Costs

Special education costs—such as tuition at schools offering autism-specific curricula—can be deductible if you can demonstrate that the program addresses documented therapeutic or developmental needs. Although these expenses often fall under disability-related deductions, official proof from a certified professional or institution is usually required.

- Assistive Devices

Assistive devices—from specialized communication apps to sensory equipment—may qualify as deductible expenses if they are medically validated by a professional (e.g., pediatrician, psychiatrist, or speech therapist). In many cantons, these costs fall under general or disability-specific medical deductions, subject to threshold rules (often 5% of net income, unless fully covered by disability rulings). Be sure to keep all prescriptions, invoices, and relevant medical certifications on file.

- Tax Deductions for Family Caregivers

If you are responsible for the day-to-day care of a person with autism—especially if officially recognized as a disability—some caregiving expenses could be deductible. This might include respite care, specialized training, or medically recommended home modifications (e.g., installing safety features or sensory-friendly adaptations). However, not every expense automatically qualifies; many cantons impose thorough documentation requirements or partial thresholds.

- Employment Status and Tax Implications as a Family Caregiver

Caring for an autistic family member can reduce your work hours and income, which in turn affects your overall tax situation. However, lost income itself is not a deductible expense. While some cantons may offer minor allowances or caregiver-specific deductions, these rarely offset the real financial consequences of cutting back on work.

International Perspectives on Autism Tax Relief

Countries worldwide handle autism-related tax benefits differently. For instance, the United States permits deductions for certain therapies once medical expenses exceed 7,5% of adjusted gross income, whereas the United Kingdom has specific tax credits for disabilities. Germany classifies many autism-related costs as “extraordinary burdens” (außergewöhnliche Belastungen), potentially reducing taxable income. While these international benchmarks offer perspective, they do not override Swiss regulations.

Switzerland in Comparison

Switzerland’s federal-cantonal system offers two main approaches for disability-related deductions:

- Lump-Sum Deduction: Calculated from the officially recognized degree of disability, this simplifies filing but may be less beneficial if your actual costs are high.

- Itemized Deductions: Allows you to list specific expenses—such as therapies, devices, and consultations—for a potentially larger deduction, provided you maintain thorough documentation.

In practice, if your overall disability-related expenses exceed the lump-sum rate, itemizing might yield a bigger tax break. If your costs are lower, however, the lump-sum could be more advantageous. Because thresholds and definitions vary by canton, it’s prudent to compare both methods before finalizing your tax return.

Final Note: Assessing the Value of Disability-Related Deductions

When it comes to disability-related tax considerations—whether for autism or any other condition—individual circumstances play a significant role. Adults with severe disabilities often have low or partial employment, which results in lower taxable income. In such cases, it may not be worth investing extensive effort to claim deductions for expenses that aren’t clearly illness-related. By contrast, an in-depth tax analysis or ruling can be beneficial for high-income families with minor children who have a disability, as these deductions could substantially reduce their tax burden.

Remember that only costs not covered by insurance are deductible. Any payments from health insurance, disability insurance (IV), assistance allowances (Hilflosenentschädigung), or supplementary benefits (Ergänzungsleistungen) must be declared and cannot be deducted again.

If you’re considering a therapeutic measure that isn’t strictly medically necessary but still appears worthwhile, contact your insurance provider beforehand to find out if they cover any portion of it. You can then seek clarity from the tax office regarding deductibility before incurring the expense.

Table of Contents

Latest blog posts

Swiss Wealth Tax 2026: What Expats Need to Know

How much wealth tax will you pay in Switzerland? Compare 2026 cantonal rates with our interactive calculator, learn what’s taxable, and see how expats can reduce the bill.

Imputed Rental Value in Switzerland: What Property Owners Need to Know in 2026

In this article, we explain what the imputed rental value is, how it is calculated, and what all you need to take into account when declaring it in your tax return.

The 3-Pillar System in Switzerland in 2026: How Pillar 3a Works, What Changed, and How to Make the Most of It

A complete guide to Pillar 3a for expats and international professionals in Switzerland — contribution limits, tax savings, 3a bank vs securities, retroactive buy-ins, withdrawal tax by canton, and cross-border implications.