Can Foreigners Buy Property in Switzerland? 2026 Lex Koller Guide

Switzerland approves roughly 1,500 vacation-home purchases by foreigners each year, and Zurich, Zug, Geneva, and Basel get zero of them. But if you hold an EU/EFTA passport and a B or C permit, Switzerland treats you the same as a Swiss buyer, and Lex Koller doesn’t apply to you at all. This 2026 guide walks through who can buy what, which cantons still have quota, what a non-resident mortgage really costs, and the three annual taxes most buyers forget to budget for.

Key takeaways

- EU/EFTA nationals with a B or C permit buy Swiss property with no Lex Koller approval. Third-country C-permit holders are treated the same as Swiss citizens.

- Third-country B-permit holders can buy a primary residence for own use. Everyone else (non-residents, foreign companies) falls under Lex Koller and competes for 1,500 vacation-home approvals per year.

- Buying Swiss property does not give you Swiss residency. Switzerland has no Golden Visa.

- Non-resident buyers typically need 35-50% down (vs. 20% for residents), and closing costs range from 0.4% in Zurich to 4.1% in Geneva on the same purchase price.

Can Foreigners Buy Property in Switzerland? The Quick Answer

Yes, most foreigners can buy Swiss property, but the rules depend entirely on your residence permit and nationality. Under the Federal Act on the Acquisition of Real Estate by Persons Abroad (BewG, SR 211.412.41, known as Lex Koller), four categories of buyer face four different rules.

EU and EFTA nationals who actually live in Switzerland and hold a B, C, or L permit are fully exempt. A third-country national with a C permit is treated the same as a Swiss citizen. A third-country B-permit holder can buy a primary residence that they themselves live in, without approval. Everyone else, non-residents, foreign-controlled companies, third-country nationals without a Swiss permit, needs cantonal approval, and approvals are largely reserved for vacation homes in a handful of tourism cantons.

The system is tighter than Portugal or Spain but more open than Austria or the Czech Republic. In 2022, Swiss cantons issued 995 Lex Koller approvals to buyers from abroad, against an annual federal ceiling of 1,500 units (Die Volkswirtschaft, 12/2023). Most European expats who’ve been here long enough to get a B permit never encounter Lex Koller at all.

| Buyer status | Primary residence | Second home | Vacation home | Commercial |

|---|---|---|---|---|

| EU/EFTA with B or C permit (Swiss resident) | No permit | No permit | No permit | No permit |

| Third-country C permit | No permit | No permit | No permit | No permit |

| Third-country B permit | No permit (own use) | Permit required | No permit | No permit |

| Non-resident / third-country L / foreign company | Permit required | Permit required | Permit required | Case-dependent |

| Cross-border commuter (G permit) | N/A (lives abroad) | Permit exempt (workplace region) | Permit required | No permit |

Do You Need a Lex Koller Permit?

Lex Koller exists to keep Swiss residential real estate from becoming a passive-investment playground for capital parked abroad. The law was enacted in 1983 and has been through several tightening cycles since, most recently the April 2026 draft revision (see below). The permit trigger is whether you qualify as a Person im Ausland under Art. 5 BewG. Whether you’re sitting in Switzerland or abroad when you sign matters less than your legal ties to the country.

EU and EFTA nationals

If you hold an EU or EFTA passport and you’re lawfully resident in Switzerland with a B, C, or L permit, you buy on the same terms as a Swiss citizen. You can purchase a primary residence, a second home, a vacation chalet, a rental building, or commercial property, and Lex Koller is silent on all of it. This is the direct effect of the Agreement on the Free Movement of Persons with the EU. The one edge case: EU/EFTA nationals living abroad, not Swiss-resident, still need approval for a vacation home.

Third-country nationals with a C permit

A C permit puts you on equal footing with Swiss citizens for property purchases regardless of your passport. American, British, Canadian, Indian, Chinese, or Brazilian C-permit holders all buy freely. The C permit comes after 10 years of continuous residence (5 for certain nationalities under bilateral treaties), so this is the path most long-term expats end up on.

Third-country nationals with a B permit

B permit holders from outside the EU/EFTA face the narrowest exemption. You can buy a primary residence that you actually live in, with no Lex Koller approval. The rules are strict: the property must be self-occupied, not rented out, not even partially. If you decide to let out a room on Airbnb or move into a different apartment, you’ve triggered the permit requirement retroactively and created a compliance problem. Tax rulings and anticipatory advice matter here.

Cross-border commuters (G permit)

French, German, Italian, and Austrian commuters with a G permit who work in Switzerland but live across the border can acquire a secondary residence in their workplace region without Lex Koller approval. The exemption exists so someone commuting three hours each way can reasonably stay overnight during the workweek. It doesn’t extend to vacation homes or to regions outside the canton of employment.

Everyone else

Non-residents, short-stay L-permit holders without proper Swiss residence, and foreign-controlled companies all need cantonal approval. In practice, approvals are granted for vacation homes in tourism cantons within the quota, for main residences where the buyer proves they will move their center of life to Switzerland, and for a narrow set of commercial exceptions. A refusal leaves no realistic workaround. Structuring a purchase through a Swiss SPV does not escape Lex Koller: Art. 5 BewG catches legal entities under foreign control.

Does Buying a House in Switzerland Give You Residency?

No. Switzerland has no Golden Visa and no residency-by-investment scheme, and the Federal Council has consistently rejected proposals to create one. Unlike Portugal’s D7, Spain’s now-closed Golden Visa, Greece’s €250,000 programme, or Malta’s passport track, a Swiss property purchase confers zero immigration rights on its own. You can own a CHF 5M lakefront villa and not be allowed to live in it for more than 90 days in any 180.

Residency has to be established through one of the usual paths: employment with a Swiss employer and a qualifying work permit, family reunification with a Swiss or EU-resident spouse, retirement with sufficient financial means (typically CHF 120,000+ annual income plus health coverage), study, or the lump-sum taxation regime (Pauschalbesteuerung) available in around 20 cantons for non-working wealthy foreigners. See our separate guide on moving to Switzerland for the full residency decision tree.

Property can support an application, for example, it can help demonstrate center-of-life when you’re arguing for a B-permit Lex Koller exemption, but the permit itself has to come from somewhere else. Getting that sequence wrong is a common mistake. We’ve seen buyers put down deposits before their work permit cleared, then sit on a property they couldn’t legally occupy full-time.

Where Can You Buy as a Non-Resident? Canton Quotas for 2026

Switzerland caps vacation-home approvals for non-residents at 1,500 units per year nationally, divided across the cantons in a schedule that has been unchanged since December 2007 (BewV Annex 1, SR 211.412.411). Nine cantons get no quota at all and simply cannot sell vacation homes to foreigners living abroad. The other 17 share the federal total, with Valais, Graubünden, Ticino, and Vaud taking the lion’s share.

Graubünden in detail: 290 units per year

Graubünden’s 290-unit annual quota under BewV Annex 1 makes it the second-largest Lex Koller allocation after Valais. The quota applies only to properties inside designated tourism municipalities (Fremdenverkehrsorte), which excludes Chur, the cantonal capital, and most of the Rhine Valley. In practice, the quota concentrates around St. Moritz, Davos, Klosters, Arosa, Flims-Laax-Falera, Scuol, and the Engadine valley. An unused allocation rolls forward one year under Art. 9 Abs. 3 BewV, and unused remainder after the following 31 October gets redistributed to cantons that have exhausted theirs.

Valais: the biggest share, and often exceeded

Valais gets 330 units a year under the Annex, and actual approvals in 2022 reached 429, well above the base quota (Die Volkswirtschaft 12/2023). That’s the carry-over mechanism doing what it’s designed to do: Valais has the strongest foreign demand (Verbier, Crans-Montana, Zermatt, Saas-Fee), so unused capacity from Graubünden or Ticino gets absorbed there. French, Italian, and UK buyers dominate the approvals.

The nine zero-quota cantons

Nine cantons are simply not on the Annex 1 table at all: Zurich, Zug, Basel-Stadt, Basel-Landschaft, Geneva, Aargau, Solothurn, Thurgau, and Appenzell Innerrhoden. A non-resident foreigner cannot buy a vacation home in any of them. The rationale is that these are either major economic centers where housing is already scarce or rural cantons without meaningful tourism demand. If you want a Lake Zurich or Lake Geneva property as a non-resident, the Lex Koller route is closed. Getting there requires establishing residency first.

How Much Can You Borrow? Non-Resident Mortgage Rules

Swiss banks lend to non-residents, but on visibly stricter terms. Where a Swiss resident can borrow 80% of the purchase price with just 20% in cash, a non-resident typically needs to put down 35-50% depending on the bank and the currency of their income (UBS). On a CHF 1.5M property, that’s CHF 525,000-750,000 of cash at closing, not the 300,000 a Swiss-resident buyer would bring. For vacation homes bought under a Lex Koller quota, banks usually cap loan-to-value at 50%, so you’re looking at 50% cash down as a floor.

Which banks lend to non-residents

UBS (including the key4 digital channel), Raiffeisen, and most cantonal banks (Zürcher KB, Banque Cantonale Vaudoise, Banque Cantonale de Genève, BKB, and others) actively finance non-resident purchases. Migros Bank handles selected cases. PostFinance is effectively resident-only. Credit Suisse was absorbed into UBS in 2023, so the Swiss big-bank landscape is now UBS plus cantonal alternatives. Specialist international brokers like Enness and MoneyPark can source non-resident deals across multiple banks when one of them says no.

The affordability rule (Tragbarkeit)

Every Swiss mortgage passes the same affordability test: total monthly housing costs must stay at or below 33% of gross income, calculated with an imputed 5% interest rate (some lenders use 4.5%), plus 1% of the property value for maintenance and ancillary costs, plus amortization down to 66% LTV over 15 years. The rule hasn’t changed in 2026. It’s deliberately punitive: actual mortgage rates might be 1.5%, but you qualify as if they were 5%. For a non-resident with foreign-currency income, banks typically apply a 20-40% haircut to reflect FX volatility, which can make a USD or GBP salary look smaller than it really is.

Fixed vs. SARON in 2026

As of early 2026, resident 10-year fixed rates sit in the 1.50%-2.05% range (UBS, Comparis). Compounded SARON plus a lender margin runs around 0.9%-1.4% all-in. Non-residents typically pay 0.5-1.5 percentage points above these levels, pushing 10-year fixed mortgages into the 2.0%-3.5% range for foreign buyers. The SNB has held its policy rate since summer 2025, and most forecasters expect long-end rates to drift modestly higher through 2026.

Planning a purchase in 2026?

Taxolution models the full tax impact of a Swiss property purchase before you sign: permit path, transaction costs, imputed rental value, wealth tax, and projected gains tax on eventual sale. Book a 30-minute consultation →

What Does It Actually Cost? Transaction Fees by Canton

Closing costs on a Swiss property range from around 0.4% of the purchase price in Zurich to over 4% in Geneva, and the gap is almost entirely the cantonal property transfer tax (Handänderungssteuer / droits de mutation). On a CHF 1.5M purchase, that’s roughly CHF 5,500 in Zurich versus CHF 61,500 in Geneva, a 10× spread driven by a single cantonal line item. For anyone indifferent between a Zug apartment and a Geneva flat, these numbers move the math significantly.

Property transfer tax (Handänderungssteuer) by canton

| Canton | Transfer-tax rate | Notes |

|---|---|---|

| Zurich | 0% | Abolished 1 January 2005 at cantonal level |

| Zug | 0% | No transfer tax; CHF 180/hour land-registry fee |

| Schwyz | 0% | Abolished |

| Bern | 1.8% | First CHF 800,000 exempt for owner-occupied primary residence (after 2 years) |

| Ticino | 1.1% | Progressive; some communes add |

| Valais | 1.0-1.5% | Progressive with property value |

| Basel-Stadt | 3.0% | Full rate regardless of use |

| Geneva | 3.0% | Casatax relief reduces the effective rate for primary-residence owner-occupiers |

| Vaud | 3.3% | 2.2% cantonal + up to 1.1% communal; many communes waive communal share for primary residence |

Notary, land registry, and mortgage deed fees

Notary fees run 0.1%-1.0% of the purchase price, scaled cantonally. Zurich is at the low end (~0.1% and often split buyer/seller), Geneva and Vaud at the high end (~0.5-0.7%, buyer usually pays in Romandie). Land registry fees add another 0.1-0.5% depending on canton, and the mortgage deed (Schuldbrief) fee is typically 0.1-0.25% of the mortgage amount. Real estate agent commission is 2-3% plus 8.1% VAT, paid by the seller in practice, so not part of the buyer’s direct closing stack.

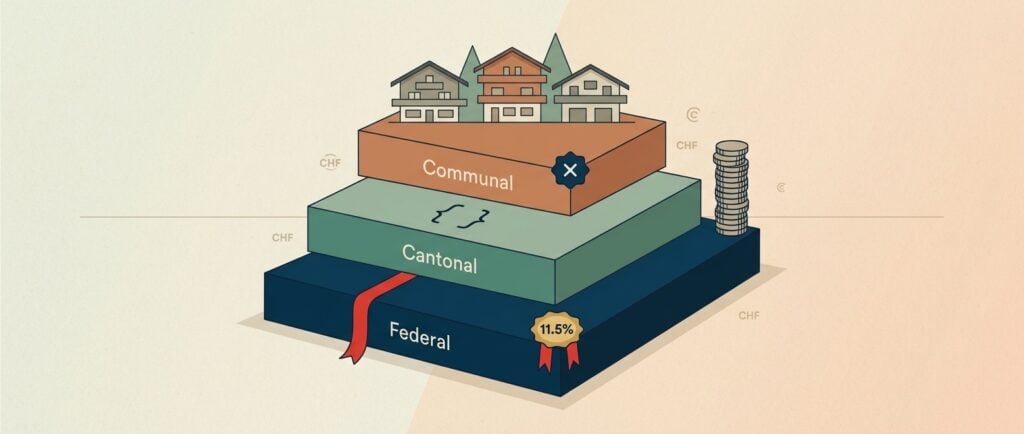

The Ongoing Tax Layer Most Buyers Forget

Swiss residence triggers tax on worldwide income and wealth, and owning Swiss property layers three recurring obligations on top of that framework, obligations real estate brokers rarely discuss and most foreign guides omit: imputed rental value (taxed as income), wealth tax on the property’s net taxable value, and a latent property gains tax (Grundstückgewinnsteuer) that sits on the property until you sell. Underestimating these can turn an apparently attractive purchase into a persistent negative carry.

Imputed rental value (Eigenmietwert / valeur locative)

Switzerland taxes homeowners on a theoretical rent they could charge if they let their home out, typically set at 60-70% of an open-market rent. For a CHF 1.5M apartment that would rent for CHF 50,000/year, the imputed rental value might be CHF 32,000, added to your taxable income, not to your tax bill directly.

What that actually costs depends on your marginal rate and your mortgage. A typical HNW expat in Zurich or Geneva sits in a marginal combined (federal + cantonal + communal) rate of 30-40% at incomes above CHF 200k. Run the math two ways:

- Cash buyer (no mortgage). CHF 32,000 imputed rental value at a 35% marginal rate = roughly CHF 11,200 in additional annual income tax, offset only by the maintenance deduction (flat 20% = CHF 6,400 → additional tax on CHF 25,600 → ~CHF 9,000/year). That’s a real, recurring cost of ownership that most foreign buyers forget to price in.

- Leveraged buyer (CHF 900k mortgage at ~2.2%). Mortgage interest of ~CHF 19,800/year is deductible against the CHF 32,000 imputed rental value. Add the maintenance flat-rate (CHF 6,400), and your deductions (CHF 26,200) almost fully offset the imputed rental, leaving CHF 5,800 net added to taxable income → ~CHF 2,000 additional tax at 35%. In many cases the deductions exceed the imputed rental, and homeownership actually reduces taxable income overall.

This is why Swiss homeowners historically don’t rush to pay off their mortgages, the interest deduction is structurally valuable while imputed rental value is in force. In September 2025, a federal referendum passed abolishing imputed rental value for primary residences, with implementation now confirmed for 1 January 2029 (Federal Council, April 2026 communiqué) and cantons expected to follow. Mortgage interest deductibility on primary residences goes with it. Until then, the current rules still apply. Our full breakdown is in the imputed rental value guide, and you can model your own exposure with the imputed rental value calculator.

Wealth tax on the property

Cantons levy annual wealth tax on the net taxable value of property, which is assessed at the cantonal Steuerwert (usually 70-85% of market value) minus any mortgage debt registered on the property. A CHF 1.5M property with an 85% Steuerwert and a CHF 900,000 mortgage gives a net taxable addition of roughly CHF 375,000, taxed at cantonal rates of 1-8 per mille depending on canton and total wealth. That’s somewhere between CHF 375 and CHF 3,000 per year for that single line item. The full cantonal comparison sits in our Swiss wealth tax guide, with a wealth tax calculator that gives you the canton-specific bill.

Property gains tax when you sell (Grundstückgewinnsteuer)

Real estate gains are taxed separately from capital gains on securities. Every canton runs its own property gains tax, it’s always cantonally administered, never federal, and the rate is progressive to your holding period. Zurich taxes a gain on a property held 2 years at ~42%; the rate falls to 20% after 20 years. Geneva and Ticino operate similar progressions. The tax can’t be planned away, but timing and maintenance-cost documentation make a real difference. More detail on the relationship between capital gains and professional-dealer classification is in our capital gains tax exemption guide.

Maintenance costs are deductible, if you document

Federal tax law lets homeowners deduct maintenance either via a flat rate (10% of imputed rental value for properties less than 10 years old, 20% for older) or via actual itemized costs. The choice can be made annually. Documenting actual costs usually wins once you’re doing meaningful upkeep, a new kitchen, a roof, insulation, a heat-pump conversion. The line between deductible maintenance and non-deductible value-adding investment matters a lot and gets audited. We cover it in depth in the property maintenance cost optimization guide.

How to Actually Buy a Property in Switzerland

A Swiss real estate transaction runs through seven discrete stages, from permit diagnosis to land-registry entry. The notary drives the middle of the process and is neutral, they represent the transaction, not the buyer. For non-residents needing Lex Koller approval, budget 2-6 additional months between signature and registration.

The seven steps

- Confirm your Lex Koller status. Identify which of the four permit tiers you fall into. If in doubt, request a written confirmation (Feststellungsverfügung) from the cantonal authority before shopping.

- Get a mortgage pre-approval. Bank affordability and LTV rules bind your budget well below asking prices. UBS, cantonal banks, and Raiffeisen all offer pre-approvals valid 3-6 months.

- Identify and inspect the property. Swiss listings sit on Homegate, ImmoScout24, and Neho; agent involvement is normal but optional.

- Due diligence. Get a building-survey report if the property is older than 15 years, check the land registry extract (Grundbuchauszug) for servitudes and mortgages, and verify the cantonal tax valuation (Steuerwert) to project ongoing tax.

- Sign the purchase contract (Kaufvertrag) at the notary. The notary prepares the deed, reads it aloud to both parties (yes, in full), and collects signatures. A deposit of 10-20% is customary at this point.

- Lex Koller approval (if required). Cantonal land-acquisition authority reviews; timelines range from 2 weeks in straightforward cases to 6 months where quota or use-conditions are contested. Approval attaches conditions and a registry note.

- Land registry transfer. The notary files the deed with the cantonal land registry (Grundbuchamt). Ownership passes on registration. Transfer tax and registry fees are settled here.

Lex Koller 2026 Revision: What’s Coming

On 15 April 2026, the Swiss Federal Council opened the formal consultation (Vernehmlassung) on a significant tightening of Lex Koller, with comments due by 15 July 2026 (Federal Council press release, 15 April 2026). The political driver is the SVP’s 10-Million-Schweiz initiative and a 29 January 2025 mandate to the Federal Department of Justice and Police. Under normal federal legislative timelines, realistic entry into force would be 2028 or later, after parliamentary debate and any referendum window.

The draft contains six substantive changes:

- Third-country B-permit holders would lose their current primary-residence exemption. They’d need approval even for an owner-occupied primary home, and would be obliged to resell within two years of leaving Switzerland.

- Foreign acquisitions of commercial property for rental or leasing purposes would be prohibited. The goal is to close a loophole where capital parked abroad buys Swiss rental buildings via corporate structures.

- Cantonal vacation-home quotas would be reduced. The current 1,500 national cap would drop, with specific new figures in the consultation documents.

- A new permit requirement for foreigner-to-foreigner resales. Currently many such transfers are permit-free if both parties are already qualifying holders; the draft closes that.

- A ban on foreign acquisition of listed Swiss real-estate company shares and of regularly traded real-estate fund and SICAV shares. This would re-subject passive investment vehicles to Lex Koller that were previously out of scope.

- A loosening for foreign-controlled hotels in tourism regions to buy staff housing without permit, subject to a two-year sale obligation if no longer used for staff.

For anyone closing a purchase in 2026 or 2027, current rules still apply. US, UK, or Asian nationals on a B permit considering a primary home should note the proposed two-year resale obligation on departure, which could meaningfully change the hold-period economics. Buyers interested in listed Swiss real-estate funds should watch the consultation closely.

Frequently Asked Questions

Can Americans buy property in Switzerland?

Yes, with conditions. An American with a Swiss C permit buys on the same terms as a Swiss citizen. With a B permit, they can buy a primary residence they themselves live in, without Lex Koller approval. Without Swiss residence, they can typically only buy a vacation home in one of the 17 tourism cantons that hold quota under BewV Annex 1, and approval is not guaranteed.

How much money do I need to buy a house in Switzerland as a foreigner?

Non-resident buyers typically need 35-50% of the purchase price in cash, plus 2-5% in closing costs depending on the canton. On a CHF 1.5M property, that’s CHF 550,000-800,000 cash at closing in Zurich; the same deal in Geneva adds roughly CHF 45,000 in transfer tax, pushing the total closer to CHF 850,000.

Does buying property in Switzerland give you residency?

No. Switzerland has no Golden Visa and no residency-by-investment scheme. Residence has to be established through employment, family reunification, retirement with sufficient financial means, study, or lump-sum taxation (Pauschalbesteuerung) in one of around 20 cantons. Property ownership can support a residence application but isn’t a path on its own.

Can foreigners get a mortgage in Switzerland?

Yes. UBS, Raiffeisen, and most cantonal banks (ZKB, BCV, BCGE, BKB) lend to non-residents. Expect stricter loan-to-value ceilings, 35-50% down instead of the resident’s 20%, and a 0.5-1.5 percentage-point rate premium. Affordability is tested with an imputed 5% interest rate plus 1% for maintenance, capped at 33% of gross income.

Which cantons do not allow foreigners to buy vacation homes?

Nine cantons have zero quota under BewV Annex 1: Zurich, Zug, Basel-Stadt, Basel-Landschaft, Geneva, Aargau, Solothurn, Thurgau, and Appenzell Innerrhoden. A non-resident foreigner can’t get Lex Koller approval for a vacation home in any of them. Buying there requires first establishing Swiss residency.

What ongoing taxes do I pay after buying a Swiss property?

Three recurring taxes: imputed rental value (taxed as income, roughly 60-70% of market rent), annual wealth tax on the property’s net taxable value (tax base minus mortgage debt, cantonal rates 1-8 per mille), and a latent property gains tax on eventual sale (Grundstückgewinnsteuer, cantonal, progressive to holding period). Mortgage interest and maintenance costs are deductible.

The Bottom Line

Three decisions determine whether a Swiss property purchase makes sense: your permit status (which governs whether Lex Koller applies at all), your canton choice (which swings closing costs by a factor of 10 and ongoing wealth tax by roughly 3×), and your financing path (resident 20% vs. non-resident 40-50% down, and the FX haircut on non-CHF income). The April 2026 revision signals tightening ahead, not loosening. Anyone on a B-permit primary-residence plan should factor in the proposed resale obligation even if the final law is still 2-3 years away.

Planning a Swiss property purchase?

Taxolution models the full tax picture before you sign: permit path, transaction costs, imputed rental value, wealth tax by canton, and projected gains tax on eventual sale. No real-estate commission, no product sales, pure tax advisory.

Table of Contents

Latest blog posts

Swiss Income Tax Rates 2026: Federal, Cantonal & Communal Stack Explained

Swiss income tax in 2026: federal brackets, the 26-canton effective-rate table at CHF 250k single and CHF 350k married, and the canton-choice CHF lever.

Swiss Property Maintenance Tax Deductions 2026: Last Window Before the 2029 Eigenmietwert Switch

Flat-rate vs actual costs, the 26-canton matrix, and the 2026-2028 last window before the Eigenmietwert switch ends federal maintenance deductions in 2029.

Swiss Lump-Sum Taxation 2026: Guide for Wealthy Arrivals

Switzerland still lets qualifying wealthy foreigners pay tax on their Swiss living costs instead of their worldwide income, and the federal floor for this regime in 2026 is CHF 435,000. For a wealthy arrival with CHF 2 million in worldwide income and CHF 15 million in net worth, ordinary Swiss tax in Vaud runs close […]