Hiring in Switzerland: What US Businesses Need to Know

Growing US companies are keen to expand their workforce by tapping into Switzerland’s skilled talent pool. Your ideal candidate could be based in Zurich, Zug, Schaffhausen, Basel, or Geneva. While the potential for talent is clear, navigating social security and tax coordination rules can be complex.

Understanding how to effectively and legally employ Swiss-based individuals helps US companies ensure compliance, reduce legal risk, and build a cost-efficient international workforce presence.

Common Challenges for US Employers

Social Security Coordination

When employing someone residing in Switzerland, US employers must navigate social security considerations carefully. Switzerland enforces strict rules to ensure all workers are appropriately insured under its national system. Fortunately, a bilateral social security agreement exists between the United States and Switzerland, which helps avoid dual coverage and contributions in many situations.

A situation where a Swiss-based employee works for a foreign employer that has no legal presence in Switzerland—such as a US-based company—is referred to as an ANobAG arrangement. The term ANobAG is short for Arbeitnehmer ohne beitragspflichtigen Arbeitgeber, meaning “employee without a contribution-liable employer.” In these cases, the employee is affiliated with the Swiss social security system, but the employer is not. This designation is central to the compliance structure discussed in this article.

ANobAG status generally applies when either the employer is not domiciled in Switzerland or the employee is not a national of Switzerland or another EU/EFTA country. In other words, if either party falls outside the scope of bilateral coordination rules (as defined under EU and EFTA social security treaties), Swiss law treats the setup as an ANobAG. This is typically the case for third-country employers such as those based in the United States.

Under the US-Switzerland Totalization Agreement, workers are generally subject to the social security laws of the country where they are physically working. However, specific provisions provide exceptions, especially for temporary assignments.

- Detached-worker rule (Article 5): A US employee sent to work in Switzerland for five years or less remains covered under the US system and exempt from Swiss coverage, provided they have a certificate of coverage from the US Social Security Administration.

- Self-employed rule (Article 6): Self-employed individuals are generally subject to the system of their country of residence.

It’s important to secure a Certificate of Coverage from the appropriate authority (in the US, the Social Security Administration) to ensure the exemption is honored by Swiss authorities.

Outside of the detached-worker context, if the employee resides in Switzerland and works for a US employer, they will usually need to be affiliated with the Swiss social security system (AHV/AVS). In such cases, it is the employee who becomes affiliated with the Swiss social security system (AHV/AVS). While the US employer is not legally affiliated, Swiss compensation offices may still require minimal cooperation from the employer—such as confirming the effective annual salary or co-signing administrative documents. However, the main responsibility for contributions rests with the employee.

Under Swiss domestic law, Article 6 of the Federal Act on Old-Age and Survivors’ Insurance (AHVG) provides a mechanism for handling these cases:

- If the employer is not subject to mandatory Swiss contributions, the employee pays the full AHV contribution of 8.7% of their gross salary.

- However, if the employer agrees, the contribution can be split equally between employer and employee at 4.35% each, provided this arrangement is documented and submitted to Swiss authorities.

This allows for a partial replication of the standard contribution split seen in domestic employment, even when the employer has no formal Swiss presence. Nonetheless, the employee remains formally liable for ensuring that contributions are handled correctly.

In practice, the salary paid to the employee under an ANobAG arrangement is typically the full gross amount. The employee is then responsible for calculating and remitting the total AHV contribution to the Swiss compensation office—including both the employee and employer shares. Since the foreign employer cannot access the Swiss system, cost-sharing agreements are typically executed via reimbursement. However, under Swiss rules, any such reimbursement is treated as part of the employee’s income and therefore increases the contribution basis.

This results in an atypical payroll structure by Swiss standards: in traditional employment, only the employee’s share is deducted from the gross salary, and the employer remits the contributions, meaning that the difference from gross to net is just the employee’s share of the contribution. In contrast, ANobAG employees must manage both parts, and their gross salary effectively functions as a “budget” from which they fulfill their entire social security obligation (employer and employee).

This mechanism places ANobAG employees at a relative disadvantage compared to EU or UK direct employment cases, where the employer is formally affiliated with the Swiss social security system. In those cases, employer-side reimbursements do not inflate the employee’s contribution base. For third-country employers like those in the US, the entire amount paid—including reimbursements—is included in the calculation base, which leads to a higher effective contribution burden for the employee, even when contractual gross salaries are identical.

Mandatory Insurances

Employees working in Switzerland are entitled to several key protections, though their access depends on the employment structure. These include:

- Accident insurance (UVG): Coverage for both occupational and non-occupational accidents. ANobAG employees must arrange this coverage themselves through a compliant Swiss insurer.

- Family allowances and unemployment insurance: These require mandatory registration with Swiss authorities. ANobAG employees must ensure they are registered individually to access such benefits.

The Occupational pension (BVG) second-pillar pension scheme is generally reserved for employees working for an employer affiliated with the Swiss social security system. ANobAG employees are not mandatorily covered by the BVG and cannot join it directly. As a result, they do not build up occupational pension benefits.

ANobAGs can, however, make enhanced contributions to their third pillar (pillar 3a), using the same rules that apply to self-employed persons. This allows them to deduct up to CHF 36,288 per year (in 2025) into a tied pension account. While this offers valuable tax savings and retirement planning flexibility, it is not equivalent to BVG participation, as it lacks employer co-contributions and the same level of risk or disability coverage.

In the absence of a Swiss legal entity, the responsibility for coordinating these insurances falls on the employee. Understanding the gaps—particularly in occupational pension coverage—is critical when weighing the long-term sustainability of the ANobAG model.

Taxation Coordination: Avoiding Double Taxation

The US-Switzerland Tax Treaty outlines how income from employment is taxed between the two countries and helps avoid double taxation. Unlike social security coordination under the Totalization Agreement, taxation does not follow an exclusivity principle. This means that an employee may become liable for taxation in both countries depending on where the work is physically performed.

According to Article 15 of the tax treaty, income from employment is generally taxable only in the country of residence—unless the work is performed in the other country. In that case, the portion of income attributable to work performed in the other country may also be taxed there.

In practice, this means that a Swiss-resident employee working partly in the US (e.g. on assignment or for meetings) can be taxed in Switzerland on their income overall—but the US may tax the portion attributable to the US workdays. The rest remains subject to Swiss tax. To avoid double taxation, the treaty allows for mechanisms such as tax credits or exemptions, which need to be applied properly through each country’s tax filing process.

Under certain conditions—such as short stays under 183 days within a 12-month period, where the salary is paid by a non-resident employer and not charged to a permanent establishment in the other country—the host country may not exercise taxation rights. However, each condition must be assessed carefully.

A common misconception is that Swiss withholding tax (Quellensteuer) applies automatically to B-permit holders. This is not the case when the employer is not domiciled in Switzerland. Instead, the employee must file an ordinary Swiss tax return to declare the income. It’s important to note that physical presence in Switzerland—not just permit status—triggers taxation obligations.

Workday Tracking and Compliance

Since taxes depend on where the work is physically carried out—not where the employer is based—it’s crucial to accurately track the employee’s workdays across different countries. Even occasional days spent working in the US (or Switzerland, for US-based employees) could lead to partial taxation in that country.

Common Pitfalls

Continuing US Payroll After Relocation

One of the most frequent missteps is continuing to process payroll only through the US after the employee has relocated to Switzerland. Even if the employment contract or payroll remains based in the US, Swiss tax authorities will typically consider the date of Anmeldung (local registration) as the start of local tax liability. Any income earned from that date onward becomes Swiss-source income. Delays in adjusting can create retroactive tax liabilities and complications in reclaiming or offsetting tax payments made in the US.

Unclear Presence and Delayed Action

Some employment situations involve a gradual or unclear move—such as remote work arrangements or commuting plans—which can lead to inaction. But tax liability is not suspended by ambiguity. Where there is uncertainty about whether the employee has “moved” or which jurisdiction has taxing rights, it is therefore strongly advised to get clarity early. In complex cases, employers or employees may seek a formal clarification or ruling from the Swiss tax authority to gain legal certainty and minimize risks of dual taxation or penalties.

Possible Solutions for Hiring in Switzerland

Note that the challenges described above primarily concern cases where a US-based company hires a Swiss resident directly (ANobAG). While this may be possible in certain worker scenarios (under the Totalization Agreement), direct employment is not always the most practical solution.

Fortunately, alternative models exist that enable compliant and effective hiring of Swiss-based talent by US companies. These include Employer of Record (EOR) solutions, and establishing a Swiss legal presence. Each route carries different trade-offs in terms of cost, administrative complexity, and long-term scalability.

Quick Recap: ANobAG (Employee Without Swiss-Accessed Employer)

- Eligibility: Applies when no other EU/EFTA bilateral rules apply – when the US employer has no legal presence in Switzerland, and the employee becomes subject to Swiss social security due to their residence and work location.

- Advantages: Enables employment without setting up a Swiss payroll or entity. The employee assumes responsibility for social security affiliation and compliance, and the administrative burden on the US employer is reduced.

- Considerations: The employee handles registration, contributions, and insurance setup. This setup can lead to suboptimal pension integration (e.g., no BVG) and higher effective contribution bases due to reimbursement mechanics. Execution also varies by canton, and employers may still be asked to support with salary confirmation or documentation.

Employer of Record (EOR)

- Eligibility: Appropriate for companies of all sizes and nationalities that want to avoid direct registration or operational involvement in Switzerland.

- Advantages: The EOR legally employs the individual on behalf of the US business. This allows full access to Swiss benefits and local compliance with minimal overhead for the US employer. It’s a turnkey solution, particularly for quick or short-term needs.

- Considerations: The EOR becomes the formal employer of record, which can complicate perception for client-facing or senior roles. Costs are typically higher on an ongoing basis. Not ideal for long-term team building unless EOR is part of a transitional strategy.

Swiss Subsidiary or Branch

- Eligibility: Best suited for companies with multiple Swiss employees, or long-term commercial goals in Switzerland.

- Advantages: Provides full legal and operational presence in Switzerland. Enables native payroll, contracting, and full participation in local social insurance systems, including BVG and UVG. Offers credibility and flexibility for scaling operations.

- Considerations: Requires notarial setup, local accounting, initial capital, and regular administrative compliance. It is a long-term investment rather than a rapid deployment option.

Comparison Table: Employment Methods

| Method | Administrative Effort | Cost | Employer Responsibility | Suitable Scenario |

|---|---|---|---|---|

| ANobAG | Low (for employer) | Low | Limited to salary payments & contracts | Non-EU/EFTA nationals, Third-state employers, lean setup |

| Employer of Record (EOR) | Minimal | Higher | Delegated to EOR provider | Quick setup, full compliance outsourcing |

| Swiss Subsidiary/Branch | High | Highest | Full local compliance & HR infrastructure | Strategic presence or multi-staff operations |

Conclusion

Hiring talent in Switzerland as a US-based company can be strategically valuable—but it comes with a distinctive set of legal, tax, and social security implications that differ significantly from arrangements within the EU or UK.

For employees based in Switzerland working for a US company without a legal Swiss presence, the employment relationship is classified under Swiss law as an ANobAG (Arbeitnehmer ohne beitragspflichtigen Arbeitgeber). This means that the employee is independently affiliated with the Swiss social security system, while the employer remains outside of it. The ANobAG model enables compliance without requiring a Swiss entity, but it places significant administrative and financial responsibility on the employee. It also leads to structural disadvantages—such as the inability to access the BVG pension system and inflated contribution bases due to reimbursement mechanics.

When international coordination complexity, or employee expectations make ANobAG unattractive, an Employer of Record (EOR) can offer a streamlined alternative. By outsourcing the formal employment relationship to a Swiss provider, the company ensures compliance across tax, social security, and labor law—though often at a higher cost and with some limitations on employer control and positioning.

For companies planning long-term growth in Switzerland, establishing a Swiss subsidiary or branch may be the most robust and scalable solution. While the setup requires time, capital, and administrative overhead, it offers full integration into the Swiss system and control over HR, payroll, and commercial activities.

Importantly, while the US–Switzerland Totalization Agreement ensures exclusivity in social security coverage (i.e. affiliation with only one system at a time), income taxation under the US–Switzerland Tax Treaty is not exclusive. Tax liability can arise in both jurisdictions depending on where work is physically performed. As such, careful workday tracking, proper payroll structuring, and proactive tax planning are essential to avoid compliance risks and prevent double taxation.

In all scenarios, early coordination is key. Employers and employees alike benefit from clear documentation, a well-chosen structural model, and support from advisors familiar with Swiss cross-border compliance.

If you’re considering hiring in Switzerland, we invite you to schedule a no-obligation consultation with our team. We’ll assess your specific setup—whether it points toward ANobAG, EOR, or entity formation—and provide clear, practical guidance on how to move forward compliantly and efficiently.

Table of Contents

Related: Before setting up the Swiss entity, review our pillar guide on the Swiss corporate tax regime — canton rate ranges, TRAF relief, Pillar Two scope, and GmbH-versus-AG.

Latest blog posts

Swiss Pillar 2 Buy-In 2026: Tax Savings, the 3-Year Withdrawal Block, and When It’s Worth It

Many pension funds advertise voluntary purchases and present attractive calculation models to interested parties. What is often not mentioned is that the voluntary purchase into the pension fund is not worthwhile for everyone and does not always help with tax savings.

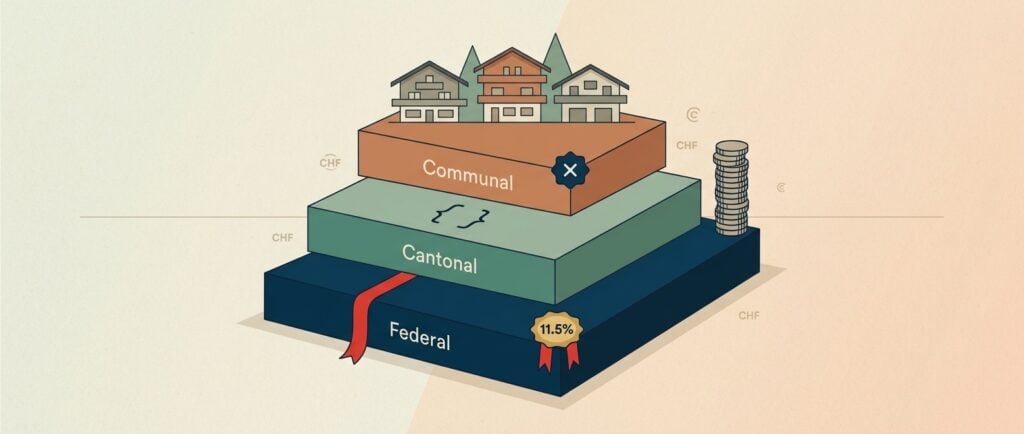

Swiss Income Tax Rates 2026: Federal, Cantonal & Communal Stack Explained

Swiss income tax in 2026: federal brackets, the 26-canton effective-rate table at CHF 250k single and CHF 350k married, and the canton-choice CHF lever.

Swiss Property Maintenance Tax Deductions 2026: Last Window Before the 2029 Eigenmietwert Switch

Flat-rate vs actual costs, the 26-canton matrix, and the 2026-2028 last window before the Eigenmietwert switch ends federal maintenance deductions in 2029.