Rent and buy property

07

Rent and buy property

The Swiss housing and real estate market varies greatly from region to region in terms of purchase and rental prices. In highly sought-after areas or larger cities, prices are relatively high, while living in rural areas is less expensive.

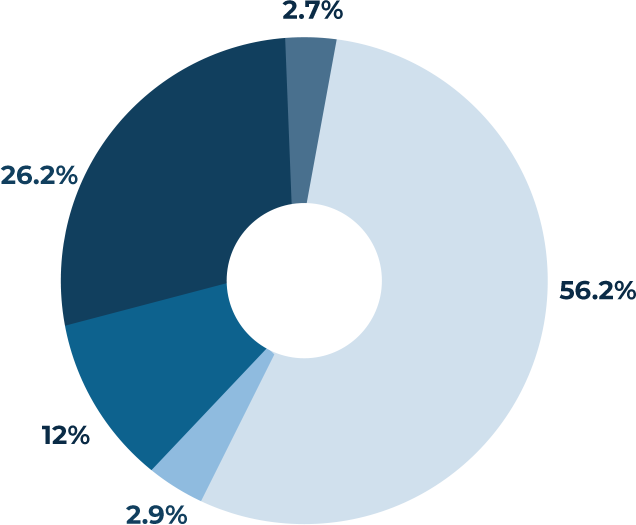

Tenant or sub-tenant

Property owner, condo owner

Member of a cooperative

Other

House owner

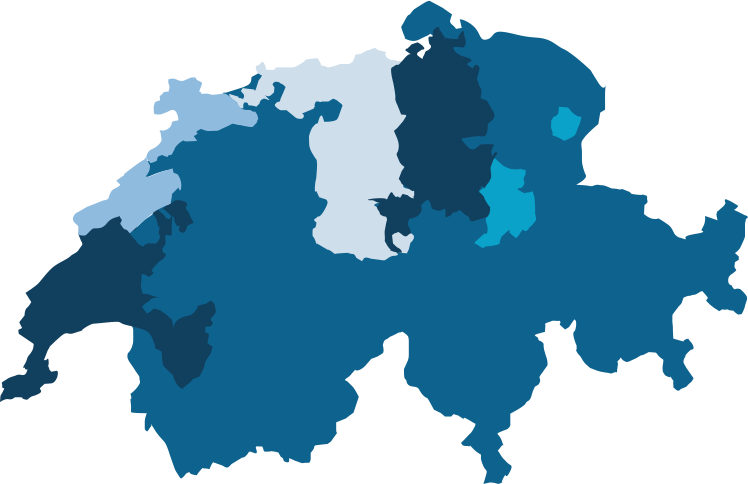

Average prices

A look at the statistics shows how different the price structure is in the various cantons.

In 2019, the square meter for a rental apartment in the canton of Zug cost an average of CHF 19.5. In the same year, one pays CHF 11.8 for it in the canton of Jura. The situation is similar for real estate purchases: In the canton of Geneva, buyers pay an average of CHF 13750 for a square meter, while in the canton of Jura, only CHF 3520 is due.

Swiss property descriptions

In Switzerland, listings describe apartments by the total number of rooms, not counting bathrooms. In some cantons, the kitchen isn’t counted either, so a four-room apartment may have two or three bedrooms and a living or dining room. Open-plan rooms that include the kitchen are often counted as 0.5 or 1.5 rooms. However, almost all adverts will list the total living space and also the total plot size for a house, giving you a clear idea of the size of the property and the garden.

Properties in Switzerland are typically without furnishings, often without even light fittings. As such, when you view the property, it is important to check whether kitchen appliances will be included or not. Laundry facilities are generally communal in apartment buildings. Tenants may have a time slot for using them.

Outdoor space is important for Swiss tenants. Many modern apartments have a balcony and often access to a communal garden or playground. Near bodies of water such as Lake Geneva and Lake Zurich, a right of access to the water will increase the cost of a property, as will the right to moor a boat.

Renting is popular

Renting a house or apartment is very widespread in Switzerland. 2.3 million households lived in a rented apartment at the end of 2019, which corresponds to a total share of 60% of households in Switzerland.

In general, the rental rate is higher in urban areas than in rural ones. In Basel-Stadt, the rental rate in 2019 was 83% and in Geneva 78% – well above the national average. In contrast, the rental rate in more rural cantons such as Appenzell-Innerrhoden was 38%.

> 1800 CHF

1600 – 1800 CHF

1400 – 1600 CHF

1200 – 1400 CHF

< 1200 CHF

Rent property – what you need to consider

Broker can help with mediation

In highly sought-after areas, it is rare for a property to remain vacant for a long time. There, rental properties are often not even published on the internet, but immediately referred by an agent or the landlord himself. So if you want to rent a property in a region that is in high demand, it is advisable to do so through a real estate agent. This can often drastically reduce the time needed to find a suitable property.

Use other sources as well

Even if you use a realtor, however, you should also go apartment or house hunting on your own to make sure you exhaust all your options and have the widest selection. Use real estate portals on the internet like homegate.ch, immoscout24.ch etc., as well as rental advertisements in local newspapers. Often, advertisements for rental properties are also posted at the municipal administration.

How to apply to rent a Swiss house or flat

Landlords seem to broadly work on a first-come, first-served system so in a competitive area you’ll want to hand in your application as soon as possible, perhaps even before you see the property. You can always withdraw your application if you don’t like the property.

Swiss rental applications are comprehensive documents. Expect to provide your:

- Age

- Marital status and number of children

- Profession and employer

- A letter of reference or indication of employment from your employer

- Salary

- Residency or visa status

- Often including copies of passports and visas

- Number and type of pets

- Duration of stay

You often must provide a document proving that you have no outstanding debts or legal judgments. This is called an extrait du Registre des poursuites / Auszug aus dem Betreibungsregister / estratto del registro dell’Ufficio delle Esecuzioni e Fallimenti.

If you’ve lived in the country for a while, make a formal request (for which you will be charged) at the nearest Office des poursuites / Betreibungsamt / Ufficio delle Esecuzioni e Fallimenti. If you’ve recently arrived, you may be able to request one from your previous place of residence, but in the first instance, you should discuss your situation with the estate agent.

Insider tip

For properties with high demand, your chances will increase if you create a nice application dossier to send to the landlord. This includes:

- A personal profile

- a letter of motivation

- possibly salary statements to support the paying power

Tenancy agreement

All tenants should have a written contract which is the tenancy agreement between landlord and tenant. This should cover:

- Rent – don’t try to negotiate, the rent is fixed in Switzerland

- Tenancy start and end date

- How and when to give notice

- Detailed property inventory

- Tenant rights to shared services

- Quiet hours

- Any other house rules.

Starting and ending a tenancy

Tenancy agreements in Switzerland tend to be for an initial period of 12 months. Traditionally, tenancies could only start or end on a quarter day which is around 25 of March, June, September, and December. This tradition continues in many areas, although its implementation is patchy. As an extra twist, the December quarter day, being Christmas, is often not acceptable for a tenancy change over. The tenant must give notice by the previous quarter day of their intention to vacate (i.e., at least three months in advance).

While this system is dying out in many areas, particularly the cities, it’s still the norm in others. This is why Switzerland has a strong sub-letting culture and tenancy transfer is common: if you can find a candidate willing and able to take over your let, you can leave at any time with little notice, even if the landlord rejects their tenancy application.

The additional costs

Service charges usually include the costs for heating and hot water consumption. Depending on the tenancy, other things may also be agreed as ancillary costs, which must also be listed in the tenancy agreement, e.g. fees for garbage collection, Internet/TV connection, garden maintenance, snow removal, etc. Incidental costs that are not mentioned in the rental agreement are generally included in the rental price. How the ancillary costs are paid is also specified in the rental agreement. A distinction is made between the payment on account and the lump-sum payment:

Payment on account

The tenant pays a certain amount for the ancillary costs in advance each month (usually this is transferred together with the rent). The landlord then prepares a service charge statement annually. Service charges that have been paid too much are then refunded. In the event of additional consumption, an additional payment is due accordingly.

At the end of the year, check the service charge statement carefully. You do not have to pay service charges for an item that is not specifically mentioned in the lease. Repairs and maintenance work may not be billed as service charges. Likewise, it is not permissible to mark an item as “other operating costs”.

Lump sum payment

In the case of lump-sum payment, the tenant also pays the service charges monthly, but does not receive a statement at the end of the year. This means that no refund is made for under-consumption, and no additional payment is due for over-consumption.

Buying residential property

Residence status decisive for real estate purchase

Anyone holding a C permit has the same rights as a Swiss citizen to purchase residential property in Switzerland – whether as a primary or secondary residence, or as a vacation home/apartment.

EU/EFTA nationals are allowed to buy a property if they have a B or C permit. For cross-border commuters (G permit), it is permitted to purchase residential property if this is for work purposes (e.g. to stay in their own property during the working week).

Costs when buying real estate

The purchase of a property must be financed from at least 20% equity, as the taking out of a mortgage is only allowed for a maximum of 80% of the purchase price.

Affordability calculator

Please note that in addition to the purchase price, you will also incur other costs:

- Notary fees

- Registration fees for entry in the land register

- Real estate transfer tax (varies from canton to canton)

- Possible brokerage costs

If you are retired and want to buy a property in which you will have your main residence, you can use your pension withdrawals from pillar 2 (pension fund) and pillar 3 (retirement pension) to pay off the mortgage.

Tax implications of the acquisition of residential property

If you buy a home, your tax situation will normally change only to a limited extent. This is because from now on, the acquired property will be added to your assets and the mortgage on it will be listed in the list of debts. This means that your taxable assets do not change significantly if you have a maximum mortgage burden.

The situation is similar on the income tax side. The imputed rental value increases taxable income. However, the mortgage interest can be declared as a deduction. It can therefore be stated that owner-occupied residential property in Switzerland that is encumbered with a mortgage has only a minor impact on the tax burden.

The situation is different if the property is not mortgaged to a large extent or even not mortgaged at all. In this case, the imputed rental value definitely leads to a higher tax burden. The same applies if the property is rented out – the rental income is fully taxable.

Latest blog posts

Is Switzerland Still a Tax Haven in 2026? How Much You Actually Pay vs the EU, UK, UAE & Monaco

Switzerland isn’t classically a tax haven, but for high earners the structural mix beats every EU comparator. Take-home and wealth tax compared to UAE, Monaco, UK, Germany, Italy, more.

Swiss Pillar 2 Buy-In 2026: Tax Savings, the 3-Year Withdrawal Block, and When It’s Worth It

Many pension funds advertise voluntary purchases and present attractive calculation models to interested parties. What is often not mentioned is that the voluntary purchase into the pension fund is not worthwhile for everyone and does not always help with tax savings.

Swiss Income Tax Rates 2026: Federal, Cantonal & Communal Stack Explained

Swiss income tax in 2026: federal brackets, the 26-canton effective-rate table at CHF 250k single and CHF 350k married, and the canton-choice CHF lever.