Moving to Switzerland in 2026: Tax Residency, Withholding Tax, and Financial Planning for New Residents

Last updated: February 2026

Moving to Switzerland is one of the more consequential financial decisions you can make. Not because the process is difficult, but because the tax and social security implications start from the moment you arrive. Switzerland’s tax residency rules kick in far earlier than most newcomers expect, your residency permit determines how your income is taxed, and key deductions are only available if you make the right decisions in your first year.

This guide focuses on what actually matters for your finances: how Swiss tax residency works, what your permit means for your tax obligations, which deductions you can claim (our Swiss tax deductions guide walks through each one with 2026 amounts), and what changed in 2025 and 2026 that affects new residents. If you need a deep dive into the withholding tax system (tariff codes, cantonal rates, voluntary vs. mandatory filing, cross-border telework rules), we published a comprehensive and updated guide on that topic: Understanding Swiss Withholding Tax (Quellensteuer): A 2026 Update.

Swiss Residency Permits at a Glance

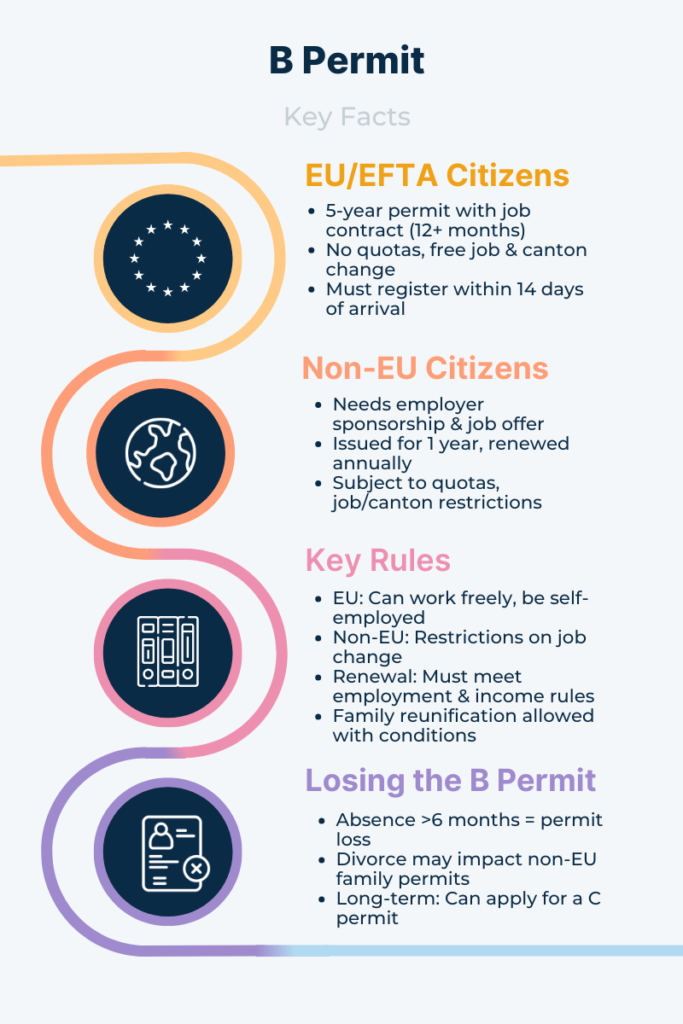

Switzerland requires all foreign nationals staying more than three months to hold a residence permit. The permit you hold determines not just your right to live and work here, but also how your income is taxed. The three main permits relevant to most expats are the L (short-term), B (residence), and C (settlement) permits.

| L Permit | B Permit | C Permit | |

|---|---|---|---|

| Type | Short-term residence | Temporary residence | Permanent settlement |

| Duration | Up to 12 months (extendable to 24) | 1 year (non-EU) or 5 years (EU/EFTA), renewable | Indefinite |

| EU/EFTA access | No quotas; for temporary stays under 1 year | No quotas; 5-year permit with 12+ month contract; free job and canton changes | After 5 years of continuous residence for EU-15/EFTA nationals |

| Non-EU access | Subject to quotas; employer sponsorship required | Subject to quotas; employer sponsorship required; usually tied to canton and employer | After 10 years of continuous residence (5 for US/Canadian citizens) |

| Tax treatment | Withholding tax (Quellensteuer) | Withholding tax (Quellensteuer) | Ordinary taxation (annual tax return) |

| Path forward | Transitions to B permit with longer-term employment | Transitions to C permit after 5–10 years | Prerequisite for Swiss citizenship |

What Matters for Tax Purposes

The critical distinction is between B/L permit holders and C permit holders. If you hold a B or L permit and are employed in Switzerland, your employer deducts tax directly from your salary each month through the withholding tax system (Quellensteuer). If you hold a C permit, or if you are married to a Swiss citizen or C permit holder, you file an annual tax return under the ordinary assessment system, just like Swiss citizens.

This distinction has real financial consequences. Withholding tax uses flat-rate deductions baked into cantonal tariff tables, which means some personal deductions (Pillar 3a contributions, pension fund buy-ins, high commuting costs) cannot be claimed unless you opt into full tax filing. We cover this decision in detail below.

For a full overview of each permit’s conditions, family reunification rules, and renewal requirements, the Swiss State Secretariat for Migration (SEM) provides current guidance at sem.admin.ch.

Swiss Tax Residency: When It Starts and Why It Matters

This is where most newcomers are surprised. Swiss tax residency doesn’t start when your permit arrives, or when you sign your employment contract, or after you’ve been here six months. It can begin as early as your first day.

The Legal Thresholds

Under the Federal Direct Tax Act (Art. 3 DBG) and the Tax Harmonization Act (Art. 3 StHG), you become a Swiss tax resident, subject to unlimited tax liability on your worldwide income and assets, when any of the following apply:

Domicile (Wohnsitz): You settle in Switzerland with the intention of remaining permanently. This is established when you register at your municipality, sign a lease, and begin living here. In practice, it coincides with your arrival date if you are relocating with the intent to stay.

Qualified stay with employment: You are present in Switzerland for at least 30 days while engaged in gainful activity. Since most people who move here to work will exceed 30 days, tax residency effectively begins on day one of employment.

Qualified stay without employment: You are present in Switzerland for at least 90 days without gainful activity. This applies to retirees, students, or people settling before starting a job.

These thresholds are far shorter than the 183-day rule used in most other countries. The 183-day concept does appear in Swiss law, but only within the context of double taxation treaties for allocating employment income between countries, not as a domestic residency trigger.

Temporary interruptions (holidays, short business trips abroad) generally do not reset the day count, provided you maintain a factual and spatial connection to Switzerland.

What Tax Residency Means in Practice

Once you are tax resident, Switzerland taxes your worldwide income and wealth. This includes your Swiss salary, but also foreign investment income, foreign rental income, foreign pensions, and other global sources. Switzerland also levies an annual wealth tax on your net assets worldwide (bank accounts, investments, real estate equity), assessed at cantonal level at progressive but relatively low rates (typically well below 1%).

Foreign real estate and certain foreign business income are normally exempt from Swiss tax, but they are still taken into account for determining your applicable tax rate (a concept called “exemption with progression”).

Tax residency typically begins on your actual date of arrival. If you move mid-year, you are a Swiss tax resident for the portion of the year from your arrival date through December 31.

How Tax Residency Is Determined in Cross-Border Cases

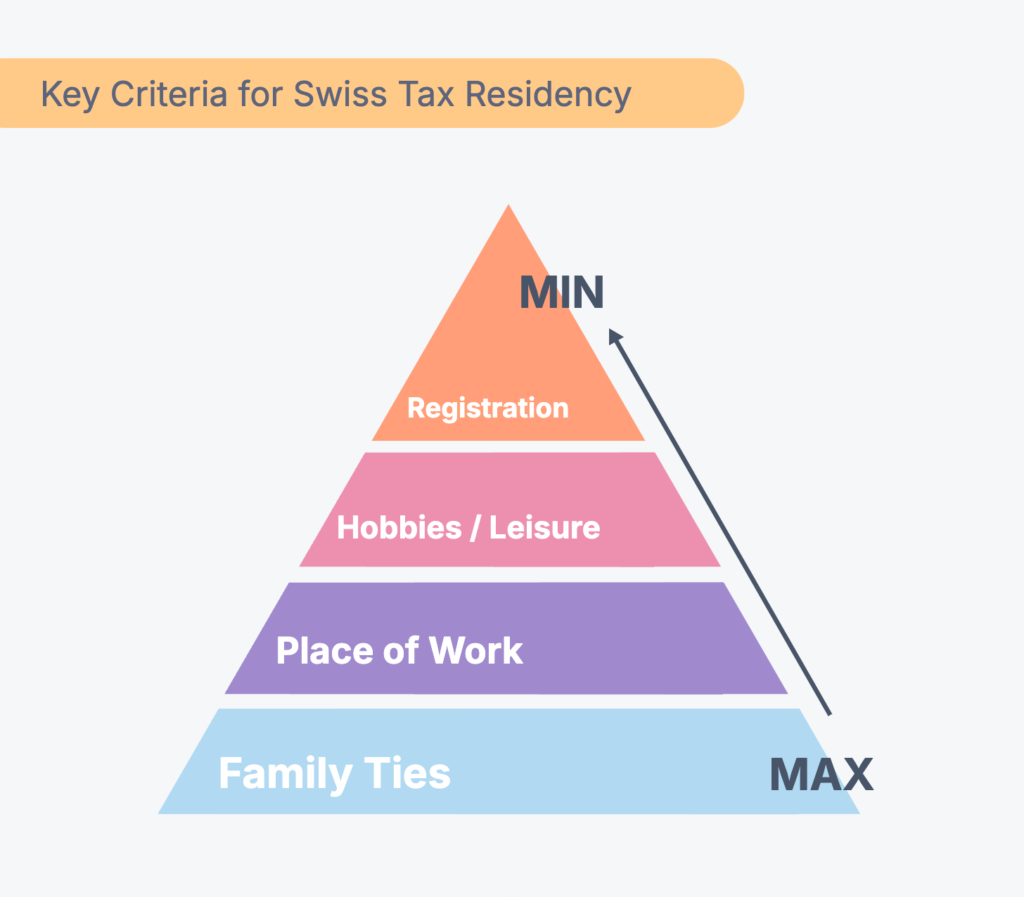

When someone could be considered tax resident in more than one country (which is common during international relocations), Swiss authorities determine the primary tax residence by examining a set of factors. Physical presence matters, but it is not the only consideration.

Hierarchy of Factors (Ranked by Importance)

1. Family ties (most important). Where your immediate family (spouse, children) lives is the single strongest indicator of tax residency. The Federal Supreme Court consistently holds that marital and family relationships outweigh even professional ties to a different location. If your family is in Switzerland, Swiss authorities will almost certainly consider you tax resident here, even if you spend substantial time working abroad.

2. Place of work. The second most important factor. If you work in Switzerland, this establishes a strong economic connection. Professional ties predominate over family ties only when they clearly outweigh all other life interests combined, which is rare.

3. Social relationships and leisure activities. Friendships, club memberships, cultural and political activities, and habitual leisure patterns are considered. These carry less weight individually but contribute to the overall picture.

4. Administrative indicators (least important). Official registration, residence permit, vehicle registration, and exercise of political rights are treated as supporting indicators, not decisive factors. Registration in Switzerland does not, on its own, create tax residency. Conversely, deregistering does not end it if your actual life center remains here.

Key Principles from Recent Case Law

The Federal Supreme Court has issued several important rulings in 2024 and 2025 that reinforce and refine these principles:

BGer 9C_496/2023 (February 2024): A landmark case involving a Swiss federal employee posted to Luxembourg. The Court held that family presence abroad outweighed the spouse’s individual work ties to Bern, and clarified that a taxpayer is not required to sever all ties with a previous residence to establish a new domicile. The focus is on the overall shift of the life center.

BGer 9C_173/2024 (December 2024): A Zurich case where spouses claimed to have moved their center of life to Graubünden. The Court upheld Zurich’s claim, pointing to patterns of cash withdrawals (18 of 22 in the Zurich area), electricity and water consumption at both residences, and family contacts. This case reinforces the intensely fact-driven nature of domicile analysis: courts look at observable behavior, not declarations.

BGer 9C_447/2024 (January 2025): A couple claimed to have moved from Ticino to Zug mid-December, but both continued full-time employment in Ticino and maintained their rented apartment there until spring. Formal registration of departure was insufficient without substantive changes in life circumstances.

BGer 9C_591/2023 (April 2024): While concerning a legal entity, this decision shifted the standard of proof for domicile from “very likely” to “predominantly likely,” potentially making it easier for tax authorities to challenge claimed domiciles. Tax practitioners expect this lower standard to influence individual cases as well.

The overall trend is clear: Swiss authorities and courts apply an intensely fact-driven analysis, weighing observable behavior over formal declarations, and the burden of proof is increasingly shifting toward the taxpayer to affirmatively demonstrate their claimed domicile.

Pro-Rata Taxation in Your First Year

If you arrive in Switzerland mid-year, you do not pay tax on a full year’s income. But the calculation is not a simple straight-line split.

How It Works

- You are taxed only on income actually earned during the Swiss-resident portion of the year, from your arrival date through December 31.

- Your income is annualized for rate purposes. The tax authorities extrapolate your partial-year income to a full-year equivalent to determine the applicable marginal rate under Switzerland’s progressive tax system. This higher rate is then applied to your actual (lower) partial-year income.

A Practical Example

You arrive on July 1, 2026 and earn CHF 60,000 from your Swiss employer in the remaining six months:

- The authorities annualize this to CHF 120,000 to determine the applicable tax rate

- The progressive rate corresponding to CHF 120,000 is applied to the actual CHF 60,000

- Result: you pay tax on CHF 60,000, but at a higher marginal rate than CHF 60,000 alone would produce

Deductions in the First Year

Effective deductions (actual expenses incurred) are declared as incurred, without pro-rating. Lump-sum deductions that are time-related, such as daily meal allowances, may be pro-rated based on the number of days of tax liability. Practice varies by canton for certain blanket deductions.

Wealth tax is assessed based on your net assets as of December 31, but the charge is pro-rated for the duration of your tax liability that year.

The annualization is performed by the tax authorities, not by you. In your tax return, you declare your actual income; the authorities compute the annualized rate.

Avoiding Dual Tax Residency and Double Taxation

When you relocate internationally, there is a real risk of being considered tax resident by two countries simultaneously. Switzerland addresses this through its network of over 100 double taxation treaties (DTAs).

End Tax Residency in Your Former Country

Before or at the time of your move, follow the proper steps to cease tax residency in the country you are leaving. This typically means deregistering, giving up your permanent home, and documenting the date your life center shifted. Many countries use a 183-day rule or calendar-year approach, so timing your move around year-end can simplify matters.

Treaty Tie-Breaker Rules

If both countries’ domestic laws claim you as a tax resident for the same period, the DTA between Switzerland and your former country provides tie-breaker provisions. These follow the OECD Model Tax Convention (Art. 4(2)) and apply a cascading hierarchy:

- Permanent home: Resident of the state where you have a permanent home available

- Center of vital interests: If you have homes in both states, residency goes to the state with closer personal and economic relations

- Habitual abode: If the center of vital interests cannot be determined, the state where you habitually reside

- Nationality: If you habitually reside in both or neither state

- Mutual agreement procedure: If none of the above resolves it

Key Treaty Differences

Most Swiss DTAs follow the OECD model closely, but there are notable exceptions:

| Treaty Partner | Key Difference |

|---|---|

| United States | The major outlier. The US–Switzerland treaty contains a unilateral US “savings clause”: the US retains the right to tax its citizens and residents on worldwide income regardless of treaty residence. A US citizen living in Switzerland remains subject to full US taxation, though foreign tax credits mitigate double taxation. |

| France | Standard cascade, but French courts have ruled that Swiss lump-sum (forfait) taxpayers may not benefit from the treaty tie-breaker, potentially leaving them exposed to French domestic-law residency claims. |

| Germany | Standard cascade, no significant deviations for individuals. The 2025 DTA amendment addresses cross-border commuter status (20% commute threshold, 45-day non-return cap) but does not alter the Art. 4 tie-breaker. |

| UK, Italy, India | Standard OECD cascade with no material deviations for individuals. |

For a deeper look at the lump-sum regime itself, who qualifies, the CHF 435,000 federal floor for 2026, the 21 retaining cantons, the Kontrollrechnung, and the specific France dispute, see our Swiss lump-sum taxation guide.

Double Tax Relief

Even when you are clearly a Swiss tax resident, you may still have foreign income (rental income from property abroad, for example) that is taxed in the source country. Switzerland provides relief through either exemption or tax credits, as arranged in each treaty, to prevent the same income being taxed twice.

How You Will Be Taxed: Withholding vs. Ordinary Assessment

Your residency permit determines which of two tax systems applies to you.

Withholding Tax (Quellensteuer): B and L Permit Holders

If you hold a B or L permit and are employed in Switzerland, your employer deducts income tax directly from your salary each month. This covers federal, cantonal, and municipal taxes in a single deduction. The rate depends on your canton of employment, marital status, number of dependents, and income level.

For many new residents, this is the entirety of their tax obligation: no tax return required, no year-end settlement.

However, there are important exceptions:

Mandatory tax return: If your gross employment income exceeds CHF 120,000 per year, you must file a full annual tax return. The withholding tax already deducted becomes an advance payment credited against your final tax liability.

Secondary triggers: Even below CHF 120,000, cantonal thresholds for non-wage income or taxable wealth can trigger mandatory filing. In Zurich, for example, non-wage income exceeding CHF 3,000 or taxable net assets exceeding CHF 80,000 (single) / CHF 160,000 (married) requires a full return. These thresholds vary significantly by canton.

Voluntary filing: You can choose to file a return even if not required. This lets you claim personal deductions (Pillar 3a, pension buy-ins, childcare, commuting) that are not captured by the flat-rate withholding tariff. But since the 2021 reform, this decision is irrevocable. Once you file, you must continue filing every subsequent year.

Ordinary Taxation: C Permit Holders and Swiss Citizens

If you hold a C permit, or are married to a Swiss citizen or C permit holder, you are no longer taxed at source. Instead, you file an annual tax return declaring your worldwide income and assets. You pay your tax bill in installments or as a lump sum after assessment.

The Transition Year (B → C Permit)

When you receive a C permit, the transition to ordinary taxation takes effect from the month following the permit change:

- Your employer continues withholding tax through the month of the permit change

- From the following month, no more withholding is deducted

- You file a full annual tax return for the entire year

- All Quellensteuer already withheld is credited as an advance payment, applied first to Direct Federal Tax, then to Cantonal/Communal Tax

- If the total withheld exceeds your final liability, you receive a refund; if it falls short, you owe the difference

Plan for cash-flow differences: under ordinary taxation, you shift from monthly deductions to annual or quarterly tax payments.

For the complete guide to withholding tax, including tariff codes, the Tariff C median salary method, cantonal rate comparisons, voluntary vs. mandatory ordinary assessment, cross-border telework rules, and the March 2026 individual taxation referendum, see our dedicated article: Understanding Swiss Withholding Tax (Quellensteuer): A 2026 Update.

Swiss Withholding Tax Checker

Find out if Swiss withholding tax applies to your situation. Four questions, a minute or two.

Need help optimizing your Swiss tax situation?

Schedule a free consultationWhat to Expect: Approximate Tax Burden by Canton

One of the most common questions from new residents is simply: how much tax will I actually pay? The answer depends on your canton and municipality, your household type, and your income level. The differences are substantial.

The tool below shows the total effective tax rate (federal, cantonal, and municipal combined) for the capital city of each canton, based on official figures from the ESTV Federal Tax Calculator. Rates assume no church affiliation. Toggle between income tax and wealth tax, select your household type, and choose an income or wealth level to see how cantons compare.

Swiss Tax Burden by Canton

Total effective tax rate (federal + cantonal + municipal), 2025 rates. Switch between income and wealth tax.

Total effective income tax rate (federal + cantonal + municipal), 2025 rates

Need help optimizing your Swiss tax situation?

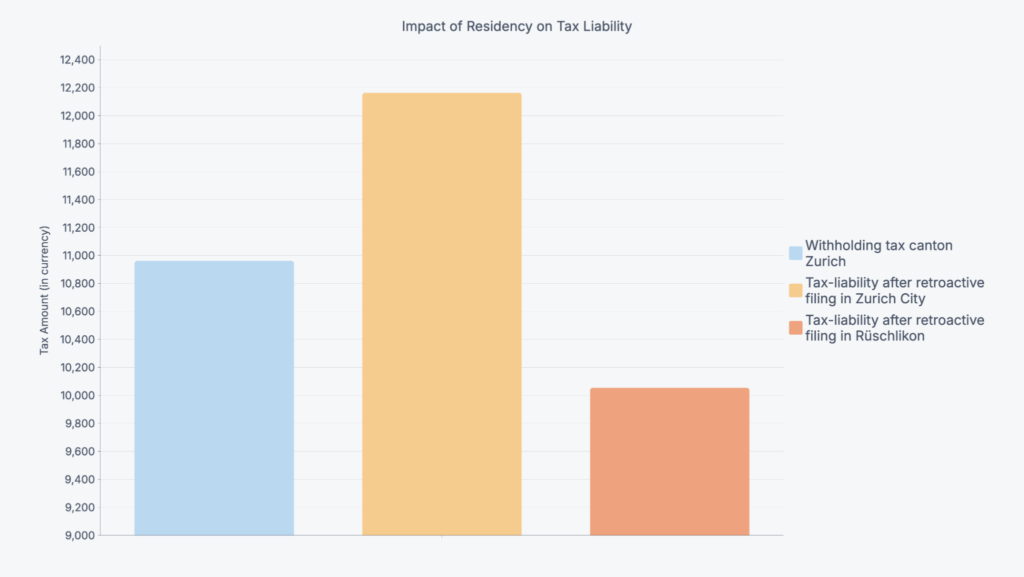

Schedule a free consultationA few things worth noting when interpreting these figures. First, these rates are for the capital city of each canton. Your actual municipality may be significantly cheaper or more expensive than the cantonal capital. Zurich-City, for example, has a higher municipal multiplier than neighboring Rüschlikon or Kilchberg, and the difference can be several percentage points at higher incomes. Second, the rates assume no church affiliation. If you are registered as a member of a recognized church (Reformed, Catholic, or Christian Catholic), expect an additional 8–15% surcharge on cantonal/municipal tax (not on the rates shown, but on the cantonal portion of your tax). Third, these rates do not include social security contributions (another ~6.4% on your payslip) or health insurance premiums. You can toggle to the wealth tax view to see how cantonal wealth tax rates compare at different asset levels.

The spread between cantons is striking. At CHF 150,000 gross income for a single person, the difference between the lowest-taxed capital (Zug, around 8.8%) and the highest (Neuchatel, around 22.3%) is over 13 percentage points, equivalent to roughly CHF 20,000 per year in absolute tax savings. For married couples with children, the gap narrows somewhat but remains significant.

Canton selection is one of the few truly controllable variables in Swiss tax planning, though it should of course be weighed against housing costs, commute times, and quality of life. Many new residents focus on the lowest-tax cantons without accounting for the fact that property prices and rents in places like Zug and Schwyz are among the highest in the country.

For a detailed look at wealth tax rates across cantons, see our dedicated guide: Swiss Wealth Tax.

What’s New for 2026

Several regulatory changes in 2025 and 2026 directly affect new residents.

Pillar 3a Retroactive Contributions (New from 2026)

Starting in 2026, you can for the first time make retroactive contributions to Pillar 3a to fill gaps from prior years. This is a significant change for retirement and tax planning, but the rules are strict:

- Only gaps from 2025 onward qualify. Contribution gaps from 2024 or earlier are permanently lost.

- AHV income required in both years. You must have earned income subject to AHV contributions in Switzerland in both the gap year and the year you make the retroactive payment.

- Current-year maximum first. You must fully contribute the current year’s Pillar 3a maximum before making any retroactive payments.

- 10-year window. A gap from 2025 can be filled at the latest by 2035.

- One payment per gap year. Each gap year is addressed with a single lump-sum payment; you cannot split it across multiple years. But you can close gaps from several prior years in a single calendar year.

- No prior withdrawal. The right to retroactive contributions lapses once you have withdrawn Pillar 3a capital.

What this means for new residents: If you relocated to Switzerland in 2025 but arrived mid-year and contributed less than the maximum, you can top up the 2025 shortfall starting in 2026. However, you cannot fill gaps for years when you were not in Switzerland, as the rule requires AHV-subject income in the gap year. If you moved here in 2026, the earliest gap you could fill retroactively would be from 2026 itself (in a future year).

Individual Taxation Referendum (March 8, 2026)

Swiss voters decide on March 8, 2026 whether to end joint taxation for married couples. If passed, every person would be taxed individually regardless of marital status. The current married-couple tariffs (Tariff B and C in the withholding system) would eventually be abolished or restructured, the child deduction would increase to CHF 12,000 per child, and the marriage and dual-earner deductions would become obsolete.

The earliest implementation would be 2032. No immediate action is required, but the outcome will affect long-term tax planning for married couples.

For a full analysis, see our dedicated guide: Individual Taxation Referendum: What the March 2026 Vote Means.

Imputed Rental Value Abolition (Eigenmietwert)

After decades of debate, Swiss voters approved the abolition of imputed rental value on September 28, 2025 with 57.7% in favor. Under the approved reform:

- The Eigenmietwert (the theoretical rental income homeowners must declare as taxable income) will be eliminated for both primary and secondary residences

- Maintenance cost deductions for owner-occupied properties will also be eliminated (including energy-efficiency renovations at federal level)

- Mortgage interest deduction will be restricted to rental properties and a declining first-time buyer deduction

Implementation is expected at the earliest from the 2028 tax period. Until then, the current system remains fully in effect. If you are purchasing property in Switzerland, plan your tax strategy based on current rules but be aware the landscape is shifting.

Geneva Income Tax Cut

Geneva reduced income tax by 5.3–11.4% effective from the 2025 tax year. This directly lowers both ordinary tax and withholding tax rates for Geneva-based workers. Middle-income earners benefit from reductions around 11%, while the highest brackets see approximately 5%. Despite the cut, Geneva remains one of the higher-taxed cantons for individuals.

Federal Tax Adjustments

Starting from the 2025 tax year (filed in 2026), the Federal Department of Finance adjusted rates and deductions for cold progression:

| Adjustment | 2025 Tax Year |

|---|---|

| Child deduction (federal) | CHF 6,800 (up from CHF 6,700) |

| Support deduction (federal) | CHF 6,800 |

| Childcare cost deduction (federal) | CHF 25,800 (up from CHF 25,500) |

| Professional training deduction (federal) | Up to CHF 13,000 |

For the 2026 tax year, the FDF has confirmed that due to low inflation, there are no further changes; deduction amounts remain at 2025 levels.

Other 2026 Changes

- Federal tax interest rates reduced: Default and refund interest dropped to 4.0% (from 4.5%); voluntary advance payment interest reduced to 0.0% (from 0.75%)

- Salary certificate guidelines updated (January 1, 2026): Flat-rate car allowance increased to CHF 0.75/km (from CHF 0.70), new CHF 600/year threshold for non-declarable gifts and event tickets, part-time status must be noted

- Pension fund deduction increased: From 6.0% to 6.5% of gross salary embedded in withholding tax tariff calculations

- Withholding tax median salary updated: CHF 5,875/month for Tariff C calculations (up from CHF 5,775)

- 13th AHV pension: Paid for the first time in December 2026 (see Social Security section below)

Tax Deductions and Planning Strategies

Tax planning in Switzerland is most effective when you start in your first year. Several key deductions and strategies can materially reduce your tax bill.

Pillar 3a Contributions

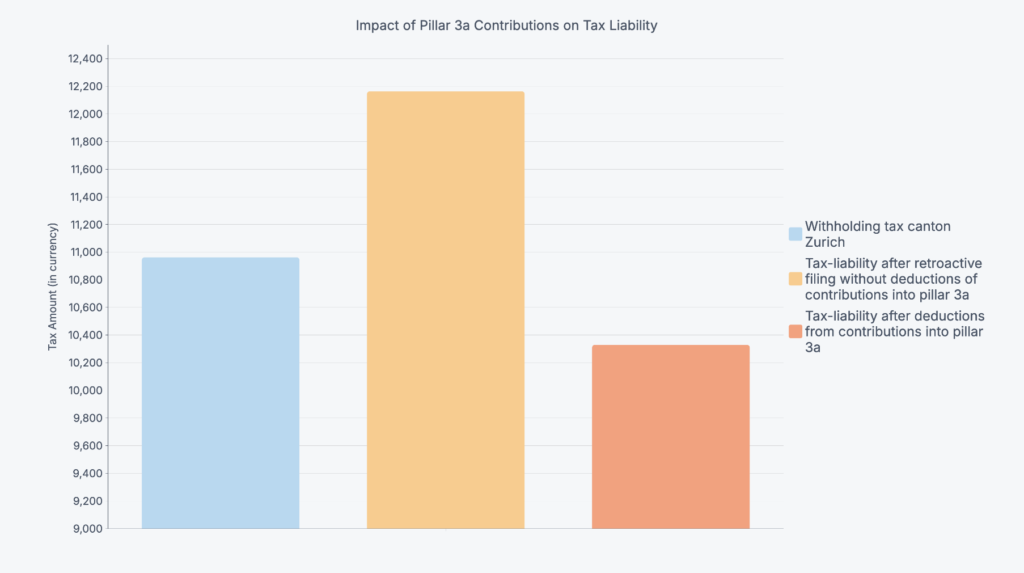

Contributing the maximum to Pillar 3a is the single most accessible tax optimization for employees. In 2026, the maximum remains CHF 7,258 for employed persons with a pension fund, or CHF 36,288 (capped at 20% of net income) for self-employed persons without a pension fund. The full contribution is deductible from taxable income at federal, cantonal, and communal levels.

If you are subject to withholding tax only (no tax return), Pillar 3a contributions cannot be deducted through the tariff system. To claim the deduction, you must either earn above CHF 120,000 (triggering mandatory filing) or request a voluntary ordinary assessment. Keep in mind that this decision is irrevocable.

Pillar 2 Buy-Ins

Voluntary buy-ins to your occupational pension fund (Pillar 2) are fully deductible from taxable income with no annual ceiling. The maximum depends on your individual pension gap, calculated by your pension fund based on age, insured salary, contribution history, and accrued benefits. This makes Pillar 2 buy-ins one of the most powerful tax optimization tools for middle- and high-income earners. Our Pillar 2 buy-in guide covers the mechanic, the 3-year withdrawal block (Art. 79b BVG), the 5 eligibility gates, and the BGer abuse jurisprudence; the Pillar 2 buy-in calculator runs the differential (your tax with vs without the buy-in) for any canton, profile, and buy-in size.

A common strategy: in years when you receive a large bonus, use part of it for a Pillar 2 buy-in to offset the higher marginal tax rate on the additional income.

Key BVG figures for 2025/2026:

| Parameter | Amount |

|---|---|

| Entry threshold (minimum salary for BVG) | CHF 22,680 |

| Coordination deduction | CHF 26,460 |

| Maximum insurable salary (BVG mandatory) | CHF 90,720 |

| Minimum BVG interest rate | 1.25% |

The proposed BVG reform was rejected by voters in September 2024 (67% against). No structural changes to Pillar 2 buy-in rules have taken effect for 2025 or 2026.

The Retroactive Filing Decision

If you earn under CHF 120,000 and hold a B permit, you face a consequential choice: stay on pure withholding tax, or opt into ordinary taxation through a voluntary assessment (nachträgliche ordentliche Veranlagung, NOV). This decision is irrevocable since the 2021 reform.

Filing can save you money if your personal deductions (Pillar 3a, pension buy-ins, childcare, commuting costs, alimony) exceed the flat-rate deductions already built into the withholding tariff. But it can also cost you money if you live in a high-tax municipality, since withholding rates use a cantonal weighted average and your actual municipal rate may be higher.

Before committing: Use your canton’s online tax calculator (e.g., the Zurich Steuerrechner) to estimate your ordinary tax burden, then compare it to your current withholding. The deadline for a voluntary NOV request is March 31 of the year following the tax year. This is a forfeiture deadline with no extensions.

Property Deductions

If you purchase property in Switzerland, mortgage interest payments are fully deductible. However, you must also declare the imputed rental value (Eigenmietwert) as taxable income. Maintenance costs can be deducted either at actual amounts or as a cantonal flat-rate deduction. Some property owners maintain interest-only mortgages to preserve the ongoing interest deduction, an approach that can be advantageous in a low-interest-rate environment. As noted above, the Eigenmietwert system is set for abolition from 2028 at the earliest.

Charitable Donations

Donations to registered Swiss charities or recognized NGOs are deductible from taxable income, typically up to around 20% of annual income. Donations must be documented and made to organizations with Swiss tax-exempt status.

Timing of Income and Deductions

If possible, consider deferring additional taxable income (bonuses, certain pension withdrawals) to a year when your overall taxable income is lower. Conversely, front-load deductible expenses (Pillar 2 buy-ins, large charitable donations) into high-income years to maximize the benefit of Switzerland’s progressive rate structure.

Social Security Contributions

Switzerland operates a three-pillar retirement system, and mandatory social security contributions begin from your first paycheck. These contributions are significant, both for their immediate impact on take-home pay and for their role in reducing taxable income.

Employee Contribution Rates (2026)

| Contribution | Total Rate | Employee Share | Employer Share |

|---|---|---|---|

| AHV (old-age/survivors) | 8.70% | 4.35% | 4.35% |

| IV (disability) | 1.40% | 0.70% | 0.70% |

| EO (loss-of-earnings compensation) | 0.50% | 0.25% | 0.25% |

| AHV/IV/EO Total | 10.60% | 5.30% | 5.30% |

| ALV (unemployment insurance) | 2.20% | 1.10% | 1.10% |

ALV contributions apply on annual salary up to CHF 148,200. There is no solidarity contribution above this threshold; it was eliminated in January 2023 after the ALV fund’s equity exceeded CHF 2.5 billion.

Your employer also matches or exceeds each of these contributions. In addition, your employer deducts contributions for your occupational pension (Pillar 2, typically 5–12% depending on your age and plan) and non-occupational accident insurance (approximately 0.3–0.5%).

Tax Impact

All mandatory social security contributions are fully deductible from taxable income. Your annual salary certificate (Lohnausweis) shows your income net of these deductions, which effectively reduces your taxable base by approximately 6.4% before any other deductions are considered.

13th AHV Pension (New from 2026)

Following the March 2024 popular vote (approved with 58.2%), AHV pensioners will receive a 13th monthly pension payment for the first time in December 2026. The amount equals one-twelfth of the total AHV old-age pension payments received during the calendar year. This effectively increases annual pension income by 8.3%.

The 13th payment applies only to old-age pensions, not to survivors’, disability, or orphans’ pensions. For a person receiving the maximum individual AHV pension of CHF 2,520/month, the additional December payment would be approximately CHF 2,520.

While this primarily affects retirees, it is relevant context if you are planning a long-term financial trajectory in Switzerland. The pension system is becoming slightly more generous, though its long-term financing remains under political discussion.

Your First 90 Days: A Practical Checklist

When you arrive in Switzerland, several administrative and financial obligations have firm deadlines. Missing them can result in penalties, retroactive charges, or complications with your permit. Here is the chronological sequence.

Week 1–2: Municipal Registration

Deadline: 14 days after arrival (or before your first day of work, whichever comes first)

Register in person at the Residents’ Registration Office (Einwohnerkontrolle) of your municipality. Online registration via eUmzug is not available for initial immigration from abroad.

Documents to bring:

- Valid passport or ID for each family member

- Rental agreement or proof of Swiss address

- Passport-sized photos

- Civil status documents (marriage certificate, family book, divorce decree if applicable)

- Proof of health insurance, or confirmation that you will provide it within three months

- Certified translations of non-EU documents may be required

The registration officer verifies your documents, enters your data into the municipal register, and forwards your file to the cantonal migration office for permit processing. You receive a registration confirmation on the spot; the biometric residence permit card follows by mail. Fees range from approximately CHF 40 to CHF 400 depending on canton and permit type.

Week 2–4: Employment Start and Social Security

When you begin work, your employer’s compensation office requests your AHV number (Swiss social security number) from the Central Compensation Office if you do not already have one. This unique 13-digit number (starting with 756) is assigned automatically; you do not need to apply separately. You will find it on your health insurance card, payslips, and can request it from your employer or cantonal compensation office.

First payslip check: Verify that your withholding tax tariff code is correct. The code should reflect your marital status, number of dependent children, and church membership. Common errors, particularly around Tariff B vs. C for married couples or the Y/N church tax suffix, can result in over- or under-withholding. Corrections must be requested before March 31 of the following year.

Month 1–3: Health Insurance

Deadline: 3 months after taking up residence

You must take out mandatory basic health insurance (KVG/LAMal) with a Swiss insurer. If you enroll within the three-month window, coverage is retroactive to your arrival date, meaning both premiums and reimbursements apply from day one. If you miss the deadline, the canton will assign you an insurer and you may face surcharges on top of retroactive premiums.

All insurers must offer the same standard benefit package for basic insurance. The only variables are premium, insurance model (standard, HMO, telemedicine-first), and deductible (up to CHF 2,500 for adults). Use the federal comparison tool at priminfo.admin.ch for unsponsored results.

Average premiums for 2026 rose 4.4% nationwide to approximately CHF 393/month. Zug is an outlier with a roughly 15% decrease, financed by a cantonal surplus. A new minimum cantonal subsidy framework for premium reductions took effect January 1, 2026.

Month 1–2: Bank Account

A Swiss bank account is practically necessary for salary payments, rent, insurance premiums, and domestic payment systems (TWINT). Most banks accept B permit holders. Required documents typically include your passport, residence permit, proof of address (maximum 3 months old), employment contract, and, for deposits above CHF 10,000, documented proof of origin of funds. Digital banks like Alpian now offer account opening via video identification.

Month 1–3: Pillar 3a Account

If you plan to contribute to Pillar 3a (and you should, as it is the most accessible tax deduction in Switzerland), open a Pillar 3a account early in the year. Contributions made by December 31 of the tax year are deductible. If you arrive mid-year, you can still contribute the full CHF 7,258 maximum for that year (assuming you are employed with a pension fund).

Summary Timeline

| Deadline | Action |

|---|---|

| Within 14 days of arrival | Register at municipal Einwohnerkontrolle |

| First payslip | Verify withholding tax tariff code |

| Within 3 months | Enroll in mandatory health insurance |

| Within 1–2 months | Open a Swiss bank account |

| Before December 31 | Make Pillar 3a contribution for the current tax year |

| By March 31 of following year | Deadline for voluntary tax filing request or tariff correction |

This guide reflects the legal position as of February 2026. Sources include the Federal Direct Tax Act (DBG, SR 642.11), the Federal Tax Harmonization Act (StHG, SR 642.14), the Ordinance on Tax Relief on Contributions to Recognised Pension Schemes (BVV 3), Federal Department of Finance cold progression adjustments, Federal Supreme Court decisions cited by BGer reference number, and official publications from SEM, ESTV, BSV, and BAG.

Tax deduction amounts and social security rates are based on official 2025/2026 publications. Always verify current figures with the relevant authority.

Related Taxolution.ch Guides

- Understanding Swiss Withholding Tax: A 2026 Update: The complete guide to Quellensteuer, covering tariff codes, cantonal rates, voluntary vs. mandatory filing, cross-border telework, and the individual taxation referendum

- Swiss Tax Deadlines 2026: Filing dates, extension rules, and payment schedules by canton

- Individual Taxation Referendum: What the March 8, 2026 vote means for married couples

- Swiss Wealth Tax: How wealth tax works and strategies for managing it

- Marriage Penalty Explained: How joint vs. individual taxation affects your tax burden

Table of Contents

Latest blog posts

Is Switzerland Still a Tax Haven in 2026? How Much You Actually Pay vs the EU, UK, UAE & Monaco

Switzerland isn’t classically a tax haven, but for high earners the structural mix beats every EU comparator. Take-home and wealth tax compared to UAE, Monaco, UK, Germany, Italy, more.

Swiss Pillar 2 Buy-In 2026: Tax Savings, the 3-Year Withdrawal Block, and When It’s Worth It

Many pension funds advertise voluntary purchases and present attractive calculation models to interested parties. What is often not mentioned is that the voluntary purchase into the pension fund is not worthwhile for everyone and does not always help with tax savings.

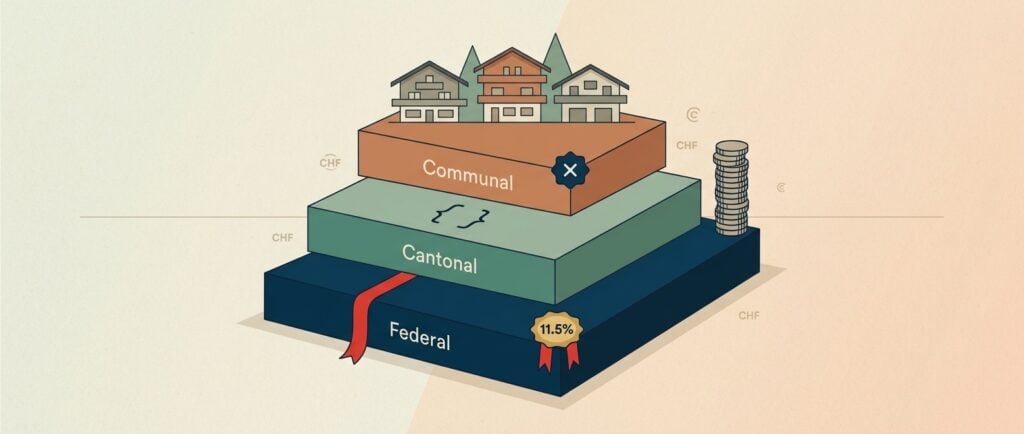

Swiss Income Tax Rates 2026: Federal, Cantonal & Communal Stack Explained

Swiss income tax in 2026: federal brackets, the 26-canton effective-rate table at CHF 250k single and CHF 350k married, and the canton-choice CHF lever.